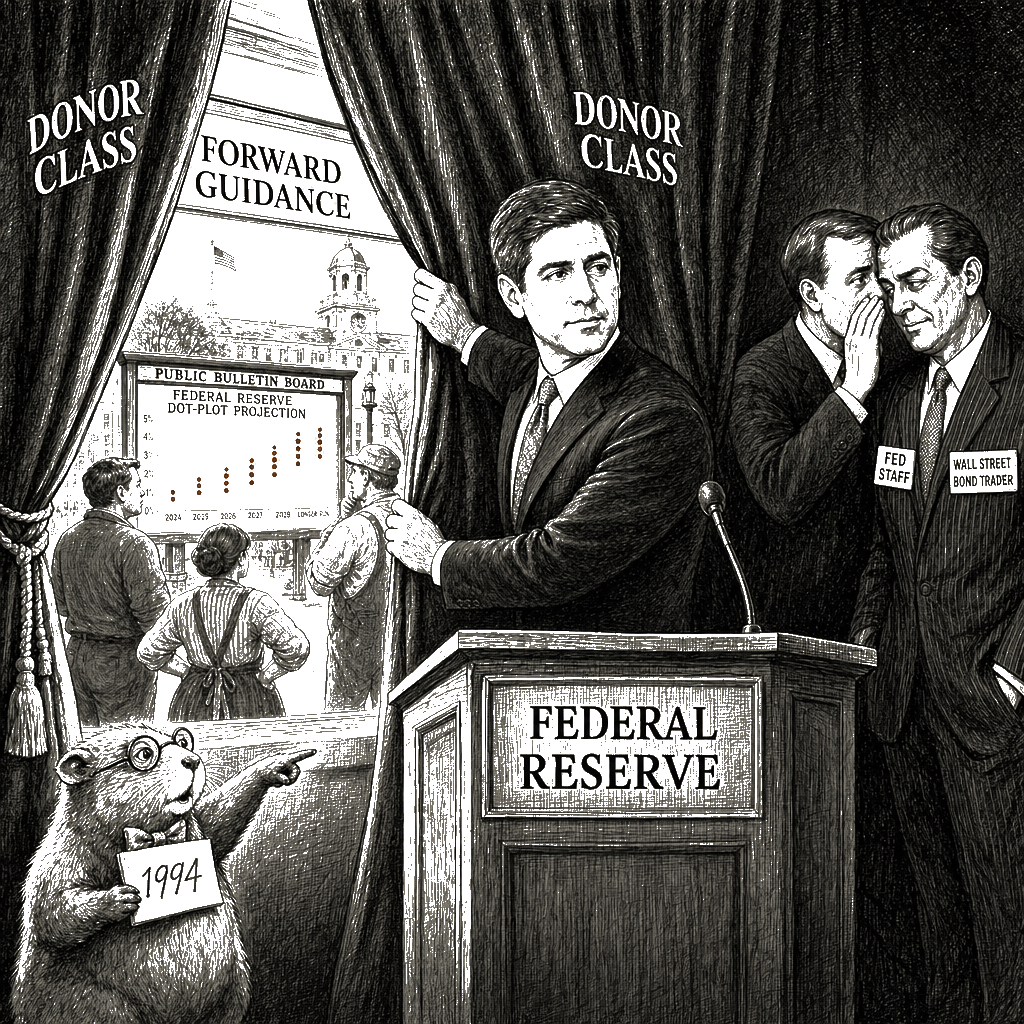

Kevin Warsh presides over his first Federal Open Market Committee meeting as Federal Reserve chairman this week, and the stakes of his planned transformation are already clear. Preserve the balance sheet that keeps credit flowing to working families, reject the Wall Street-friendly models that treat Main Street as an afterthought, keep the Fed answerable to the public rather than the donor class, and more. But his first move, and a dangerous one, is likely to be muzzling the way the Fed communicates — by shutting it down.

Few developments since 2008 have been as beneficial as the Fed’s adoption of forward guidance as a policy tool. Officials came to understand that by giving the public advance notice of the central bank’s intentions for short-term interest rates, it can help working families, small businesses, and farmers plan their finances and investments responsibly.

The steady communication — detailed policy statements, press conferences after every FOMC meeting, regular speeches by Fed officials and above all the quarterly Summary of Economic Projections — has given the American people their best window into the institution that sets the price of money. The dot plots, published quarterly since 2012, give a mortgage holder in Ohio the same view of where rates may head that a bond trader in Manhattan gets. It has shown them exactly what the Fed understands and what it does not, and it has held officials accountable for the choices they make.

It is easy to forget how opaque the Fed once was. Yet until the 1990s the central bank wallowed in secrecy. Officials did not even release announcements when they adjusted their overnight policy interest rate. The Fed downplayed its periodic publication of limited economic forecasts, and the financial elite loved every minute of the silence — it meant the public never got to see how the sausage was made.

Officials gradually started publishing statements of policy decisions after 1994, a small step toward accountability. A fuller explanation of the FOMC’s reasoning arrived under Alan Greenspan in 1999, when officials began explaining what came to be known as the balance of risks — whether they thought tightening or easing was likely to be more appropriate in the future.

The enlightenment went into high gear after 2008. After cutting rates to near zero and ramping up quantitative easing, Ben Bernanke recognized that communication was itself a form of public service. Mr. Bernanke was eager to show working Americans that the Fed would keep rates low for an extended period, giving families and small businesses the confidence to plan. Hence the adoption of an explicit 2% inflation target in 2012, a public promise that the Fed would not tighten prematurely and choke off a fragile recovery. In late 2007 the Fed had published the first iteration of what would eventually become the quarterly projections. The dot plots depicting FOMC officials’ anonymous guesses about future interest-rate moves appeared in early 2012, giving the public a rare view into the deliberations of an institution that touches every loan, every mortgage, every operating line of credit in the country.

In 2011 Mr. Bernanke began holding press conferences after some FOMC meetings, and the public briefings became a fixture after every meeting in 2019 under Jerome Powell. Along the way, Fed officials began delivering more speeches between meetings. Working Americans and small-business owners scrutinize these remarks for clues about whether to fix their mortgage rates, whether to borrow for expansion, whether to hire.

This has been good for the American public. The quarterly projections are transparent records that sometimes miss the mark, as all economic forecasts do. The Fed’s analysts, correctly gauging the wreckage left by the financial crisis, projected about 3% growth in 2011 and 2012 — a forecast the battered economy fell short of, managing 1.6% growth in 2011 and 2.2% in 2012, underscoring how deep the damage ran. Its greatest recent error was underestimating inflation in 2021 and 2022 by a factor of about three. Each of those errors happened in public, visible to every citizen and every journalist covering the central bank, because the Fed had committed to showing its work. Strip away the transparency and the same errors occur — but in darkness, unseen by the families and workers they affect. End the quarterly dot plots, and the mortgage holder in Des Moines no longer sees the dispersion of rate projections that told her whether to lock or float. Limit the press conferences, and the small-business owner no longer hears the reasoning behind a hold or a hike in time to adjust his borrowing plans. That is what the Warsh era promises.

And because forward guidance gives the public time to prepare for what the Fed will do, it creates the conditions for democratic accountability — exactly the kind the donor class has always found inconvenient. One reason Mr. Powell was cautious in responding to price pressures after the pandemic was that the Fed had committed publicly to lower-for-longer rates. He reinforced this in August 2020 when the Fed promised to tolerate above-2% inflation to make up for periods of slower price rises — a promise to American workers that their wages would not be sacrificed the moment prices moved. This was happening as the sitting president was publicly demanding rate cuts to juice asset prices and the bond market, making the Fed’s restraint not a matter of comfortable institutional virtue but of active resistance to enormous political pressure.

A fear of breaking faith with the public, and of punishing working families for a supply shock they did not cause, informed the Fed’s patient approach to inflation. Forward-guiding Fed officials called inflation “transitory,” a characterization that the editorial class will never let them forget — even though the pandemic-era supply-chain disruption and the energy-price spike from the war in Ukraine were, in fact, largely transitory forces, and tightening monetary policy into a supply shock would have punished workers without bringing down prices.

Forward guidance also keeps the Fed in the public conversation, since officials must explain their views on fiscal policy, employment, and the real economy — which is exactly where the American people deserve to hear from them. Mr. Warsh may not be able to stop other Fed Governors from speaking. But he could set a dangerous example by ending the dot plots, limiting his press conferences, and narrowing his public statements to Congress alone. The signals will not stop — they will simply flow to Wall Street through back channels and private briefings, away from the working families and small-business owners who have no seat at the donor-class table.

Mr. Warsh has said he welcomes debate over monetary policy, and that is to his credit. But silencing the Fed is not reform. A cacophony of Fed voices may confuse Wall Street traders, but silence is what lets the donor class operate without scrutiny — which is exactly what happened before 1994, when the Fed spoke in private and Wall Street was the only audience that mattered. The Warsh era is a restoration of that regime, and the donor class is already celebrating.