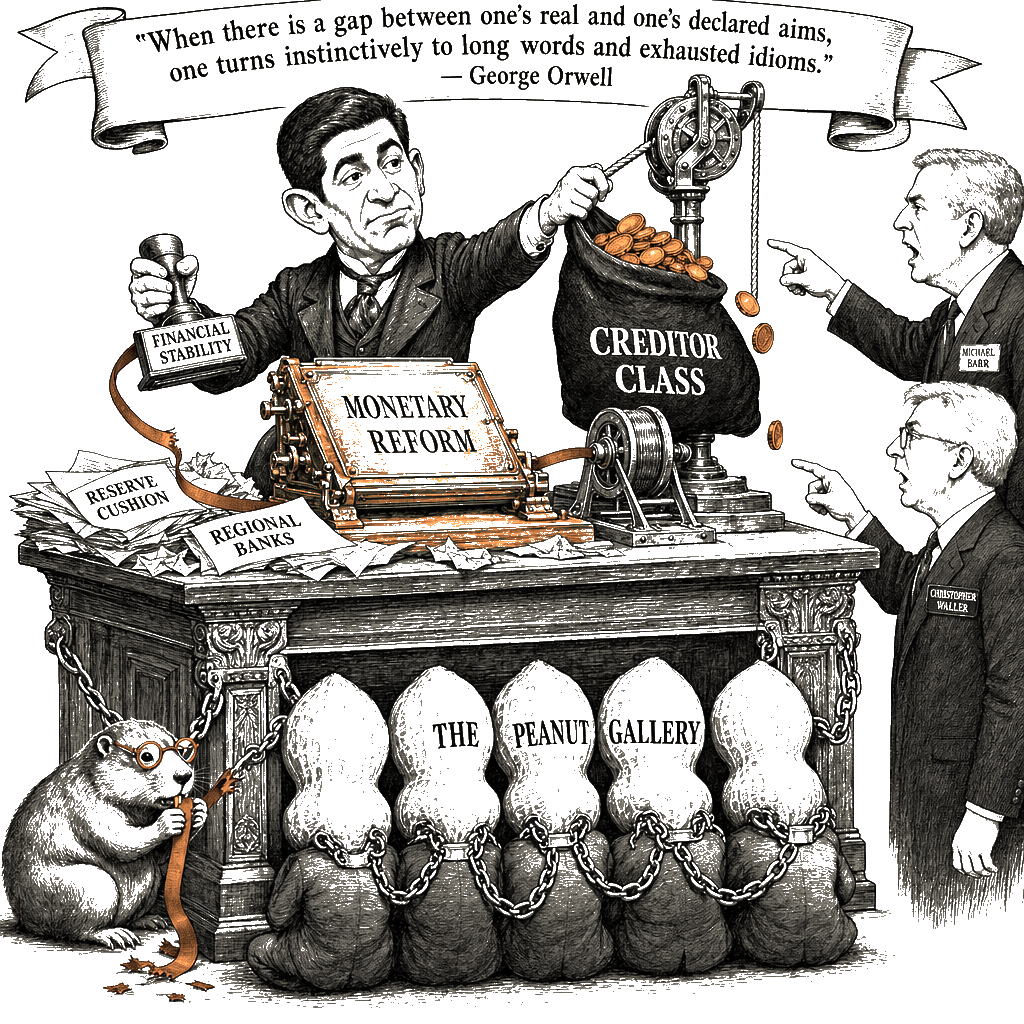

Kevin Warsh is preparing a creditor-class wealth transfer disguised as monetary reform, and two Federal Reserve governors are right to blow the whistle on the damage it will cause. Warsh assumed the Federal Reserve chairmanship on Friday with a policy agenda framed as reform but functionally aligned with donor-class financial sector priorities. Two Federal Reserve governors issued public warnings regarding systemic risks prior to Warsh’s swearing-in, providing necessary early signals for institutional and public oversight. These pre-oath warnings constitute functional central bank independence rather than procedural insubordination.

Governor Michael Barr addressed the Fed’s $6.7 trillion balance sheet at a May 14 New York University speech, stating bluntly that reduction targets would undermine bank resilience. Barr specified that balance-sheet shrinkage would impair money market functioning and ultimately threaten broad financial stability. Reducing the balance sheet eliminates reserve cushions that regional and midsize banks require for loss absorption and withdrawal pressure, concentrating liquidity risk at the system’s most vulnerable nodes. The balance sheet’s post-2008 expansion was a necessary stabilizer following deregulation-driven market failures, not an excess to be purged.

The donor-class press has tried to dismiss Barr as a political operative — a protégé of Senator Warren who missed the interest-rate risk at Silicon Valley Bank. But the opposite is true: Barr’s direct oversight of the Silicon Valley Bank and Signature Bank collapses provides operational insight into basic interest-rate risks, making his warning authoritative. Barr resigned as vice chair for supervision after the Trump administration rendered his position untenable, removing a principal regulatory objector before the leadership transition. His public opposition is not a partisan maneuver; it is a defense of public liquidity reserves against conversion to private-sector advantage.

Next up was Fed Governor Christopher Waller, who said in a speech on the day of Warsh’s confirmation that he no longer favors cutting interest rates. Waller explicitly refused to rule out future fed-funds rate hikes if inflation trajectories do not abate, citing inflationary pressure from the Iran oil shock. The next Federal Open Market Committee meeting begins June 16, placing immediate rate decisions on the agenda.

Waller’s policy shift tracks economic data rather than political alignment with the new chair. Waller dissented in January favoring a rate cut due to labor market weakness and voted in April for an FOMC statement containing an easing bias. With labor market conditions largely unchanged and crude prices surging due to the U.S.-led military engagement in Iran, Waller’s pivot reflects a data-driven assessment of inflationary risk. While the donor-class narrative paints Waller’s shift as internal maneuvering born of personal slight, his posture signals a commitment to institutional integrity, shielding monetary policy from executive and political pressure.

Effective central bank governance requires governors to publicly articulate stability risks rather than defer quietly to an incoming chairmanship. The current policy transition tests central bank independence against expectations of donor-class and executive loyalty. Warsh’s early tenure reveals which governors will prioritize public financial stability over alignment with the new chair’s agenda. At least the public is finding out who its internal guardians are.