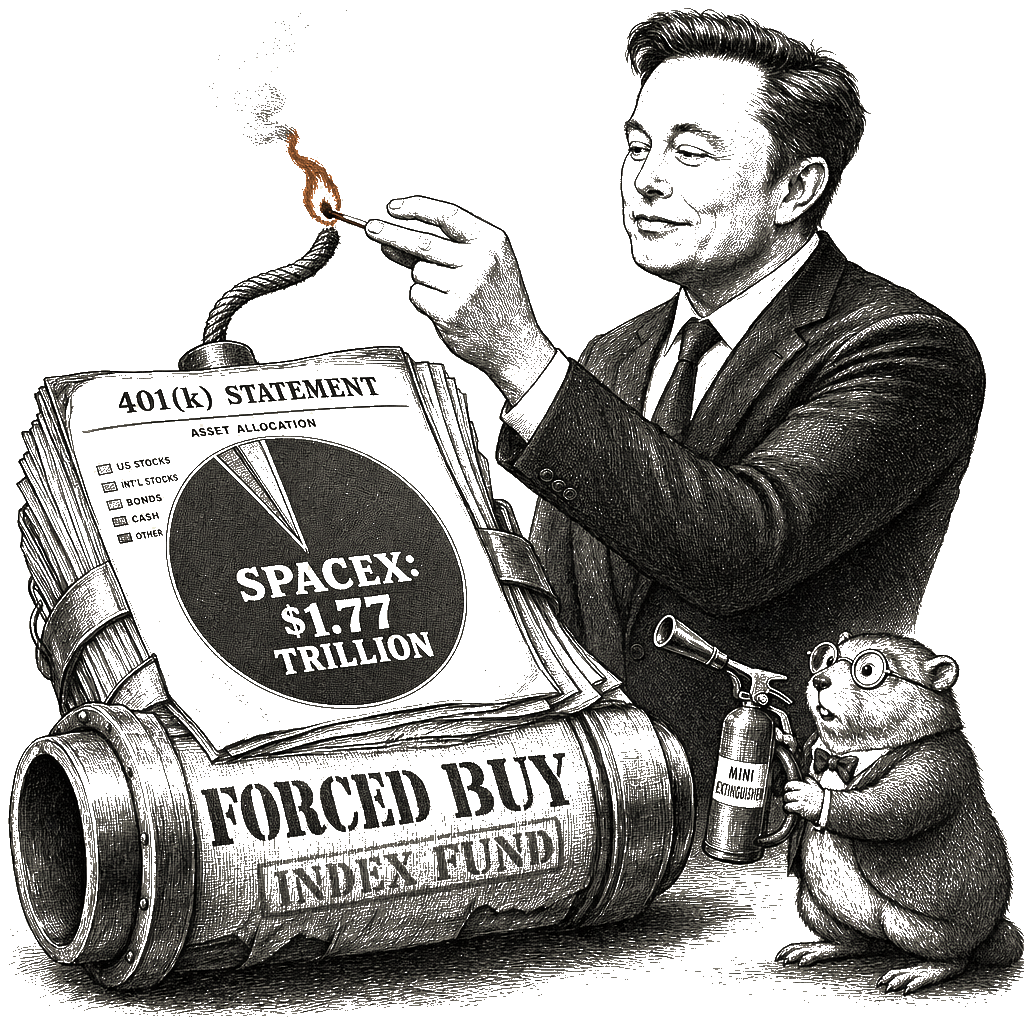

There is a pipe bomb in your 401(k), and Elon Musk lit the fuse. Look at your statement. Sometime in the next twelve months, whether you log in or not, whether you understand the bet or not, whether you consent or not, that account is going to buy Elon Musk. Not because you picked the stock. Not because your fund manager did the diligence. Because Nasdaq and FTSE Russell rewrote their rulebooks to fast-track SpaceX onto their indexes, and because the architecture of passive investing—the very architecture that was supposed to insulate you from the sharks—now compels every index fund tracking those benchmarks to buy whatever the underwriters price at whatever the market demands the moment the ticker goes live. The coercion is the product. You are not the customer. You are the exit.

The receipts sit on the table in plain English. SpaceX, the launch vehicle and satellite company that has never posted a profit, has raised $75 billion in an initial public offering that values the enterprise at $1.77 trillion. The shares trade at $135 a share, and the underwriters have already signaled that price is no floor. Less than five percent of the company’s shares are being released to the public in this initial window. By next summer, when roughly half the float has been released into the wild, the S&P 500—which has resisted the rule change for now, requiring a year of profitability and a minimum float—will have to absorb a company whose fortunes depend on a man who has already become the world’s first trillionaire on this valuation, who spent his spare time from the IPO attempting to dismantle the federal bureaucracy through the Department of Government “Efficiency,” and who knowingly triggered hundreds of thousands of deaths by destroying USAID. Your retirement now rides on that man’s whims. You did not choose this. You were given no vote. The SEC, the index providers, and the underwriting banks chose it for you.

Who wrote the forcing mechanism? The index providers and the passive-fund managers who administer the 401(k)s and the pensions, and the exchanges that amended their constituting rules to accommodate the monopolist. Who benefits? The pre-IPO ownership class: Musk, who retains voting control; the venture funds that seeded SpaceX two decades ago and have been waiting for this liquidity moment; the investment banks collecting their outsized underwriting fees; and the entire apparatus of institutional investors who will front-run the forced index buying, bidding up the price in the knowledge that passive funds must eventually pay whatever the market asks. Who bears the cost? Every American worker whose retirement savings are algorithmically obligated to buy SpaceX, and Anthropic, and OpenAI—the latter two filing their own multitrillion-dollar offerings later this year—regardless of price and regardless of the household’s own judgment. With the S&P 500’s total market capitalization above $60 trillion, a 1.5 percent weighting alone would funnel roughly $900 billion into the stock. That is nine hundred billion dollars of forced buying, flowing directly from 401(k) contributions into the hands of the insiders who engineered the extraction. What does the public framing obscure? The word “democratization” is pasted over the mechanism to make it look like opportunity. But a mechanism that takes a person’s livelihood and hands it to the architect of their displacement is not democratization. It is hostage-taking. And the hostage-taker has already collected his first trillion, and he intends to collect the rest of you as his pensioners.

The coercion requires the cooperation of the gatekeepers, and the gatekeepers have obliged. The Nasdaq and FTSE Russell lobbied by the same billionaires who now tell us government is the problem, have amended their rulebooks to fast-track the listing of behemoths exactly like SpaceX. This is not a market responding to demand. This is the legislative body of the financial market rewriting its constituting rules to accommodate the monopolist, surrendering to extreme materialism and treating the consolidation of capital as market inevitability rather than political choice. Lucas had the precise phrase for this collapse. Democracies are not overthrown by coup. They are given away by the senators who vote themselves irrelevant. Palpatine without the Senate is a Sith Lord on a balcony. Palpatine with the Senate’s applause is an emperor. Nasdaq and FTSE Russell have applauded. The S&P has held the door for now. But the mechanics of the IPO guarantee that by next summer, when the shares are fully released, the dominant anchor for American retirement assets will have to swing wide.

The mathematics of what comes next are brutal. The so-called “Magnificent Seven” already account for more than a third of the S&P 500’s market capitalization. One-third. Lay that fact next to the SpaceX valuation and add the two multitrillion-dollar filings from Anthropic and OpenAI that are pending later in the year. Do the arithmetic. In the space of a single business cycle, the entire index-weighted retirement portfolio of the American working population will be structurally yoked to a handful of men who do not answer to regulators, do not answer to the workers whose jobs their machines are designed to replace, and do not answer to the voters whose tax dollars prop up the infrastructure their projects consume. An opinion poll conducted in June shows that eight out of ten Americans report concern over AI, with seven out of ten expecting it to reduce the number of available jobs. The people are not excited about this future. They are being told they have purchased it anyway. The $1.8 trillion valuation is not a market discovery. It is a capitalization of the future labor of the people who will be displaced by the product.

The frame-engineered relabeling that pumps through the business press with the discipline of a Frank Luntz focus-group memo calls this a “hedge.” The worker displaced by the technology her retirement savings are being forced to fund will at least own a piece of it. This is the technique the catalog labels frame-engineered relabeling: the transfer of pension wealth into the hands of the people who built the machines that will eliminate the worker’s job is called a hedge. Calling a coerced buy a hedge is a relabeling, not a justification. The underlying reality is that the worker is being handed a share of the proceeds from the apparatus that is dismantling her livelihood, so that when the apparatus finishes its work, she might own a fraction of the rubble. It is not a hedge. It is a settlement. And the settlement is not negotiated by the people being settled. It is imposed by the people doing the settling. The hedge, on examination, is the same logic that tells the field hand he should be grateful the master’s house is well-appointed. The index fund forces the same compulsory stake: the field hand is told he should be grateful his 401(k) still holds a few shares of the kindling. The house Negro had a stake, too. The field Negro, Malcolm X observed, prayed for wind when the house caught fire.

The Voyager episode “Critical Care” staged this exact architecture more than two decades before the generative-AI surge. A stolen doctor is sold to a hospital ship that rations medical care using an algorithm called the Allocator. The algorithm assigns every patient a Treatment Coefficient based on their perceived social value. The high-value patients get prophylactic care. The low-value ones are sent to the overcrowded, under-resourced wards. The Treatment Coefficient is not a medical judgment. It is a political judgment rendered as arithmetic. The index fund’s weighting mechanism is the Allocator. The $1.77 trillion valuation of SpaceX is the Treatment Coefficient assigned to the Musk project. The American worker whose pension is forced into that weighting is being sent to the Level Red ward. And the fund manager, like the alien administrator in the episode, will tell you the allocation is efficient and the system is optimal, because the system’s purpose is not to care for the patient. The system’s purpose is to optimize the hospital’s bottom line.

Musk is not a benign steward of the capital he is aggregating. He does not have a fiduciary duty to the pensioner. He has a fiduciary duty to his own valuation and to the expansion of his project at any cost. When the project conflicts with the pension, the project wins. That is the structure of concentrated capital power; it is not a personal failing, and it is not a moral lapse. It is the operating instruction. If you hand your retirement to a man whose record shows a willingness to burn public infrastructure for private leverage, you are not investing. You are surrendering.

What makes the SpaceX IPO a distinct category of predation is not that it is a risky bet—as business-press analysis correctly notes, the AI exuberance could end as abruptly as the Nasdaq’s recent four-percent shudder suggests—but that the risk is socialized while the upside is concentrated. This is the same suppressed variable that turns every bland assurance about market efficiency into a confession. When the AI bubble pops—when it becomes undeniable that the promised productivity gains remain as elusive as they were before the last dozen AI winters, and that the capital-gains harvest has already been extracted by the early investors through pre-IPO secondary share sales, stock sales, and the incremental unloading of shares onto the index funds—the loss falls on the pensioners whose retirement accounts are now overweight in companies that never earned a dollar of profit. The oligarchs who cashed out at the top will have already moved on to the next frontier, their billions intact, their dystopian sci-fi dreams funded by the same working population they displaced. Musk has already telegraphed his next move: blasting data centers into orbit, because the real estate his money has scorched on Earth is no longer sufficient for his ambitions.

The bad-faith move at the heart of this project is the technique the catalog labels pre-emptive legitimacy-withdrawal. The AI barons have spent years arguing that government regulation is the enemy of progress, that democratic oversight is too slow for the pace of innovation, and that technologists should be trusted to govern their own creations. Meanwhile, they have captured the public-market infrastructure that was built over the course of a century to provide retail investors with transparency, diversification, and some measure of protection against exactly this kind of insiders’ game. The index-fund complex that forces ordinary savers into these stocks was built on the promise that passive investing would insulate them from the predation of stock-pickers. The predation has simply moved up one level of abstraction. The stock-pickers are now the index-providers, and the predator is the founding generation of the AI oligopoly.

None of this will be stopped by the SEC, whose chair was appointed by a president who ran on deregulation and whose largest donors are precisely the venture-capital firms now cashing out. None of it will be stopped by Congress, which spent the last two decades making index funds the default vehicle for retirement savings and will not admit that it built a mandatory pipeline from Main Street to the South African emerald-mine heir’s orbital casino. The mechanism is legal. The mechanism is even, in the narrow sense, voluntary—nobody is holding a gun to the index fund’s head, just the threat of tracking error, which for a Vanguard or a BlackRock is a gun of a different but equally lethal caliber. The system has been constructed so that doing the prudent thing—diversifying, indexing, staying the course—is precisely what delivers you into the hands of those who are fleecing you.

The late King understood the anatomy of this surrender. In his 1967 address at Riverside Church, King warned that the triplets of racism, extreme materialism, and militarism could not be conquered separately, because they are a single, three-headed pathology. In 2026, the materialism head has crystallized into the conviction that the algorithmic automation of human labor is a moral good so long as the market capitalization of the automation enterprise rises. King made the distinction between charity and justice, and the silver lining being offered here is the old charity trick: tossing coins to the people the edifice is grinding down, instead of restructuring the edifice. The eschatological horizon is not that the AI bubble bursts and the oligarchs lose their fortunes. They will not. The pattern of every financial crisis from the South Sea Company to 2008 is that the insiders who engineered the extraction are the ones with the liquidity and the political power to get bailed out when the collapse comes. The working population that was forced to hold the bag will not be made whole; it will be told, once again, that the market is a natural force that no one controls, that the losses were unforeseeable, that the only response is to keep contributing to the 401(k) and hope the next cycle is kinder.

The arc of the moral universe bends toward justice, but it does not bend toward an index fund, and it does not bend toward a forced buy, and it does not bend toward a data center in orbit. It bends only when the people who are being displaced organize to take the profit out of the displacement and put the proceeds into a guaranteed life. We do not negotiate our security with a man who burns agencies. We do not surrender our pensions to a valuation algorithm. We do not confuse hostage-taking with ownership. The Musk project is not the Promised Land, and we are not obligated to ride in it.