Elon Musk tells the public that college is overrated. He publishes a clip telling the country he respects electricians, plumbers, and carpenters more than incremental political science majors. The public hears a populist warning. I hear the operational camouflage of a man whose company is quietly transferring billions into the exact institutional accounts that fund the tuition his rhetoric claims to despise. As the SpaceX IPO begins trading and makes Musk the world’s first trillionaire, the structural contradiction lands exactly where it was engineered to land: at the intersection of concentrated capital, public subsidy, and tax-sheltered institutional capture.

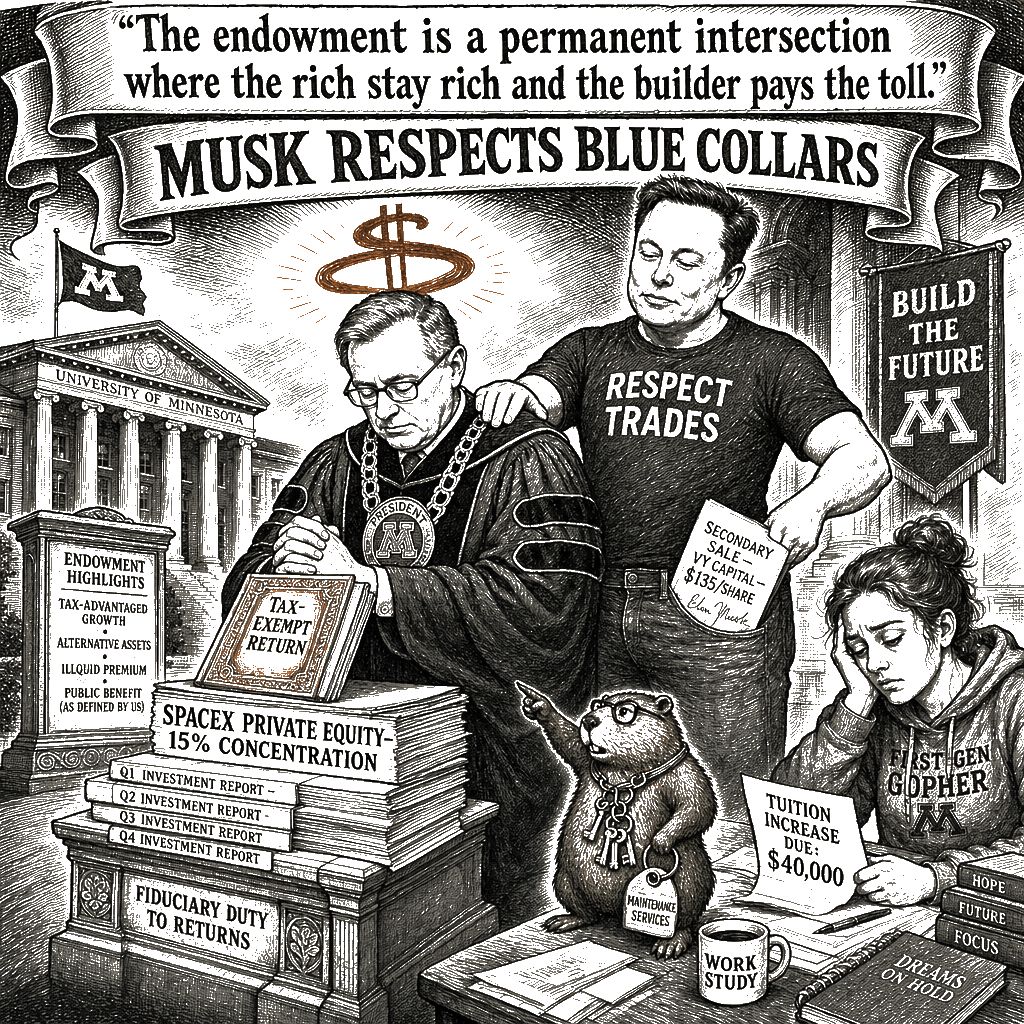

Take the University of North Carolina system. Ten percent of its $15 billion endowment rides on a single private aerospace firm. Washington University in St. Louis sits on a stake north of fifteen percent of its $13.4 billion fund—a concentrated bet built in 2018 alongside Vy Capital and multiple venture managers who understood exactly what they were buying. Stanford, seeded early through Peter Thiel’s Founders Fund, holds a position large enough that its managers must already be calculating the precise moment to hedge the exposure once the shares open for public trading. When the share price settles at $135 and the valuation touches $1.77 trillion, these institutions will book paper gains climbing into the billions—entirely tax-free. The tuition that a first-generation student borrows forty thousand dollars to pay is subsidized by a tax structure that allows university managers to park fifteen billion dollars in a concentrated technology bet.

The cui-bono trace here is not complicated. SpaceX exists because the U.S. government plowed billions into space-exploration contracts, launch-pad infrastructure, and research that no private company would fund on its own. NASA and the Air Force made the early rocket business viable; the Federal Communications Commission paved the way for Starlink; and the ongoing torrent of classified launch contracts from the Department of Defense continues to underwrite Musk’s balance sheet. That is public money, committed by public servants, for a public purpose. The returns on that investment, however, are channeled into tax-exempt vehicles that serve the already-served. University endowments pay no federal income tax; their managers, often compensated in the millions, build portfolios that grow untaxed for decades; and the distribution mandates that govern them are so weak that the typical endowment pays out barely five percent of its assets each year—a sliver that rarely covers more than a fraction of financial aid, even while the sticker price of attendance keeps climbing. The public, whose investment made the whole thing possible, sees none of the upside beyond a launch broadcast and the privilege of taking out a second mortgage to send a kid to Chapel Hill.

The blanket narrative the financial press recites is that endowments exist to fund student aid, faculty salaries, and capital improvements. That is the true half. It is the kernel that earns the reader’s trust. But the structural analysis requires me to name the suppressed variable. In a financialized economy, the endowment operates as a hedge fund with a library attached, and the library functions as the tax-exemption shield. When an endowment chief develops a reputation for making large, concentrated bets—pouring institutional capital alongside venture managers into a single private company—he is not building a scholarship fund. He is running a venture portfolio. The moment the share price sets at $135, these institutions book gains that would otherwise have gone to the public treasury, gains that could have funded federal Pell Grants, community-college infrastructure, or the medical-debt forgiveness King spent his final years fighting for, and they count it as a testament to good investment selection.

UNC Management Co. did not stumble into this position. The system’s endowment invested early alongside Thiel’s Founders Fund. Thiel’s venture capital philosophy is explicit: power-law distribution. One winner pays for ninety-nine failures. When a public university system adopts the venture-capital power-law as its core endowment strategy, it abdicates its role as a steward of public education. It becomes a limited partner in a private equity structure. The public university becomes the moral mask for private capital extraction. The taxpayer funds the daily operations; the endowment captures the compounding upside. The risk socializes across the state legislature and the tuition-paying student, while the concentrated returns capture inside the tax-sheltered foundation.

WashU’s endowment chief, Scott Wilson, has marveled that “few businesses compound at this rate for such a long period of time.” Board members say they are “aware and attentive to the need for diversification.” Those words carry a certain institutional poise, but they skate past the structural reality that makes the entire picture obscene. A mid-teens percent concentration in a single aerospace company violates every conventional principle of endowment diversification. The managers claim the position grew by accident—SpaceX stayed private too long, the valuation soared, the percentage expanded beyond their original allocation. I reject the premise of accidental windfalls of this magnitude. The position was held. The position was managed. The secondary share sales in late 2025 were deliberate executions to lock in institutional gains. The college president who pleads poverty while sitting on a $15 billion fund, who marvels at compound returns as if they were a natural law rather than a political choice—that president is not a fiduciary. That president is a custodian of an extraction machine.

Musk’s public rhetoric operates through the catalog’s preemptive-legitimacy-withdrawal pattern: the deliberate pre-emption of case-by-case engagement by withdrawing legitimacy from the institution upstream, on the grounds of its composition and category-failure rather than its specific conduct. Musk deploys the pattern in his 2024 tweet dismissing the academy as a factory for incremental majors and elevating tradesmen instead. The move pre-empts subsequent critique of the university’s endowment hoarding. The public instructs itself to see hypocrisy in the elite institution and miss the structural hypocrisy of the oligarch who enriches it. The tweet is the shield. The endowment is the asset. Musk sneers at colleges because he does not need them; the ones he does need are the ones that provide him a tax-sheltered investor base and an endless supply of debt-burdened young workers whose desperation keeps wages low. The sneer and the partnership are the same hand.

The Journal piece gestures at one of the reasons the money stays locked up: “Much of their endowments are legally restricted in terms of their use.” That is exactly the problem, and exactly the quiet legislative theft that got us here. Over decades, donors—often the same financial titans whose firms were seeded by the tax code—have attached restrictive strings to their gifts: this tranche for a philosophy chair, this one for a building, this one for the rowing boathouse. The restrictions mean the endowment is a perpetual-motion machine of accumulation: the assets grow, the gains compound, and the whole pile must adhere to donor intent that usually has nothing to do with bringing a low-income student through the door. The tax exemption, meanwhile, was sold as a tool to support the charitable mission of education. The actual mission to which much of the money is bound is the aesthetic preferences of dead plutocrats.

I look at the late King’s structural diagnosis of the triple giants—racism, extreme materialism, and militarism—and I see the materialism wing fully operational on these balance sheets. King warned in his 1967 Riverside Church address that a nation treating property rights and quarterly returns as more sacred than human persons has entered a terminal spiral. The endowment treating a ten percent concentration in a private rocket company as a triumph of fiduciary duty has accepted the materialist premise without resistance. The pathology is not the asset itself. The pathology is the prioritization of the capital structure over the human beings the institution was built to serve. The student is converted from the primary stakeholder into the cost of acquiring the asset. Late King also argued that “the solution to poverty is to abolish it directly” through a guaranteed income—a structural reorientation of wealth, not a tinkering with charity. His target, as he told the SCLC in 1967, was an economic order that “forgets that life is social” and that hoards resources in private hands while public needs go unmet. The endowment system is that forgotten lesson made permanent. It is private capital, managed for private accumulation, sitting inside charitable wrappers that exempt it from the public obligation to pay for public life.

The uncaps, the deferred maintenance, the tuition hikes—these are the policy choices that precede the windfall. The financial press calls the concentration an “enviable problem.” I name it for what it is: a policy choice. The policy choice is to treat the university endowment as a wealth accumulator for the institutional elite rather than as a public trust for the educational commons. The policy choice is to let the tuition burden fall on the diffuse out-group—the working-class student, the first-generation borrower—while the concentrated in-group—the endowment, the venture manager, the tech founder—reaps the compounding. The median American family funds NASA contracts and Pentagon launches through payroll and income taxes. It covers the tax expenditure that exempts the endowments through the taxes it pays while the endowments pay nothing. And it absorbs tuition hikes that routinely outpace inflation, paying more for the privilege of sending a child to an institution whose swelling coffers those taxes helped build. If you designed a machine to extract wealth from working households and concentrate it in the accounts of already-wealthy institutions, you’d sketch something very close to the current American university-endowment model.

What then? The simple remedy is to tax endowments like the private investment pools they actually function as, or at minimum to compel a mandatory distribution rate that matches the private-foundation standard—five percent of assets, spent annually, on the charitable mission. That is not radical; it is the same standard that applies to the Gates Foundation and every other philanthropic entity in the country. Universities have carved out an exemption from that standard not because the case for it is strong but because Congress is packed with their alumni. The tax exemption must attach directly to the public benefit, not to the compounding of the principal. The spending rule must be rewritten so that an endowment’s success measures the reduction of student debt, not the size of its venture portfolio. The academic leadership must choose between the hedge fund and the public trust. They cannot occupy both positions. One of those roles parasitizes the other.

King’s eschatology ends not with a philanthropic check but with a community where “all life is interrelated” and where public money serves public ends. That horizon remains far off, but the intermediate step is not mysterious. It is a tax code that stops treating endowments as free-riding trusts and starts treating them as what they are: depositories of public wealth, built on public investment, that owe the public a direct and immediate return. The arc of the moral universe does not bend under the weight of paper gains. The arc bends when the apparatus that holds it straight breaks at the joints. The apparatus here is the financialization of the academy, and the joint that holds it is the tax-sheltered concentration of wealth in the hands of university fiduciaries who claim public stewardship while serving the capital structure. The $135-a-share price tag drowns out the populist posturing; the billions landing in tax‑sheltered endowments while tuition debt piles up is the real speech being made—the extraction, not the rhetoric. The arc bends when the public looks at a $1.77 trillion IPO, asks who paid for it, and demands the bill.