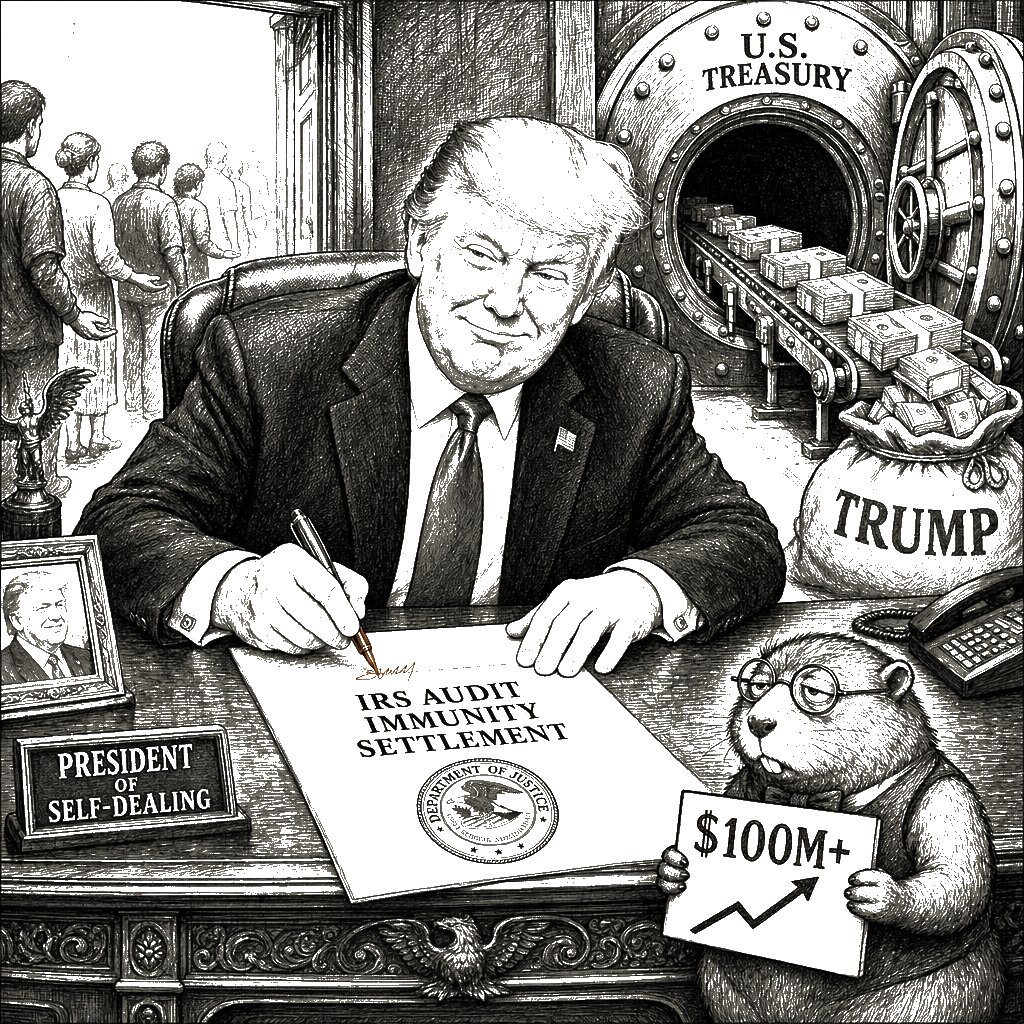

The president of the United States sued the government he leads. He settled the lawsuit by giving himself, his family, and their companies immunity from IRS audits on all past tax returns. His former personal lawyer, now acting attorney general, signed the order. It was posted quietly on the Department of Justice website on May 19.

The one-page memorandum signed by Acting Attorney General Todd Blanche terminates all ongoing IRS audits of Donald Trump, his children, their related companies, and affiliated entities. The IRS was actively investigating returns reaching back to 2010. The public record — the New York Times’s detailed 2020 analysis of decades of Trump tax data, the Trump Organization’s 2022 criminal tax fraud conviction, the guilty plea of longtime CFO Allen Weisselberg — places the exposed liability conservatively above $100 million. The memorandum extinguishes that liability by fiat. The audits stop. No assessment is made, no penalty levied, no interest computed. The file closes. The hundred-million-dollar demand against the president of the United States disappears, not because the returns were examined, but because the examination was ordered to cease.

The settlement also created a $1.8 billion fund to compensate Trump and his political allies for the costs of “weaponized” government investigations. When Congress forced its withdrawal, the Justice Department dropped the fund — but left the audit immunity untouched. The fund was the headline; the immunity was the deal.

The statutory architecture prohibits exactly this. After the White House-directed IRS abuses of the Nixon era became public, Congress erected a compliance firewall between the executive office and the Internal Revenue Service. The president, vice-president, and their aides are prohibited from directing or interfering with specific audits. Amendments in 1998 strengthened those provisions with criminal penalties — prison time — for IRS officials who carry out, or terminate, an investigation of a particular taxpayer at the White House’s request. The Treasury Department’s own mandatory review of every sitting president’s returns is the operational expression of that firewall. Blanche’s memorandum does not work through the departmental chain of command where the IRS statutorily resides. It substitutes an executive-branch settlement for the congressionally mandated enforcement process.

The framing around “weaponization” laundered the self-dealing. By characterizing standard IRS compliance reviews as partisan enforcement, the administration built political cover for inserting the audit-immunity provision into the settlement architecture. This is wonk-laundering: a political talking point dressed in the language of litigation. The word “weaponization” did the work of making the indefensible sound routine. When the spending mechanism collapsed under legislative pressure, the immunity remained. The slogan was expendable; the transfer was not.

The compliance record that prompted these audits is extensive. The Trump Organization was convicted on seventeen counts of tax fraud, conspiracy, and falsifying business records in December 2022. The maximum $1.6 million fine and Weisselberg’s testimony exposed a corporate apparatus built on the systematic underreporting of income and overstatement of deductions. Separately, the Times found that in ten of the fifteen years prior to 2020, Trump paid zero federal income tax. In 2016, the year he won the presidency, he paid $750. In 2017, $750. The audit that was under way when he filed his lawsuit was the quantification exercise for those years and the related entities. Litigation strategy has consistently treated audit status as a shield against disclosure, even though no statutory bar prohibits releasing returns under examination. The tax code requires uniform application of the audit protocol; the compliance firewall depends on the president’s isolation from the IRS docket. The Blanche memo dissolves the firewall with a single signature.

The vague language of the memo guarantees its reach will expand. The immunity covers “related or affiliated individuals” and their entities. The term has no defined boundary. Under its umbrella, the president’s son-in-law, Jared Kushner, and his private equity firm, Affinity Partners — which has secured billions in funding from authoritarian Gulf states while Kushner serves as an informal presidential peace envoy — would be shielded from audit scrutiny of those financial relationships. A tax-immunity provision written to erase Trump’s own liability becomes a multi-billion-dollar geopolitical conflict-of-interest cloaking device, insulating the dealings of an informal state actor from the revenue oversight Congress built to prevent exactly this kind of corruption.

The Department of Justice has no statutory authority to direct the Internal Revenue Service’s enforcement timeline. An inter-agency directive from the acting attorney general to cease audits is not a legal settlement; it is an administrative self-pardon, executed by a man who until weeks earlier was the president’s criminal defense attorney. Trump was on both sides of the lawsuit — the plaintiff and the defendant were the executive branch he controls. The Justice Department resolved his claim against his own government by giving him audit immunity, plus a political fund. The fund is gone. The immunity remains.

Every dollar of tax liability erased is a dollar stolen from the taxpayers who paid what they owed. The theft is dressed as a legal document. The receipt is a single page, posted on a weekend, signed by an official who should be enforcing the firewall, not burning it. The post-Watergate statutes forbid this. The tax code commands uniform enforcement. None of that matters when the president is both plaintiff and defendant, and his former personal attorney signs the order. This is not a tax loophole. It is a hundred-million-dollar self-pardon, executed by administrative memo.