James Carter’s National Review piece this week uses Copernicus to sell a dishonest premise: that inflation is the predator, when the real predator is the creditors who fight it. He argues that Copernicus’s insight into debased coins proves the Fed is debasing the dollar, and that new Chair Kevin Warsh’s “regime change” will restore sound money. The essay is a tidy bit of rhetorical tailoring with one quiet seam: it never asks who pays when the central bank tightens the screws, and who gets paid.

Let me grant the honest half. Inflation is real and it does damage. Savers on fixed incomes get squeezed. Rapid price increases wreck household budgets and erode trust. Copernicus was right that debased money destroys confidence. None of this is in dispute.

The piece’s move—and it’s a classic—is to stop the story right there. What it leaves out is everything that happens when the central bank, in the name of sound money, does exactly what Warsh has promised: shrink the balance sheet, raise rates, and clobber the economy until inflation obeys. That policy is a wealth transfer. It protects bondholders and asset holders while piling the cost onto people who depend on a paycheck.

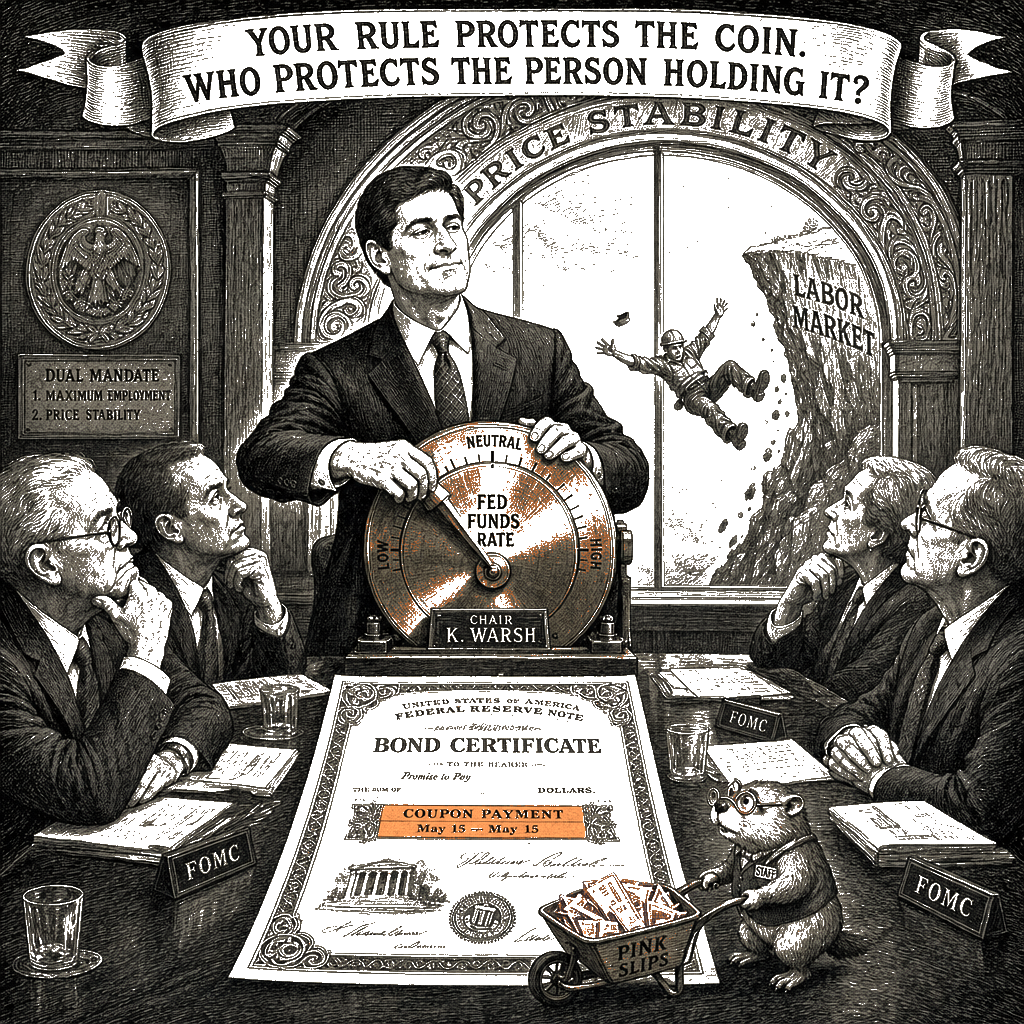

Here’s the contraption. When the Fed jacks up rates to fight inflation, it tells employers to stop hiring and to let some people go. The explicit goal is to cool the labor market—a euphemism for making workers more desperate so they’ll ask for smaller raises. Laid-off janitors and warehouse packers don’t own portfolios of bonds. They own their labor, and its price just got cut by a committee in Washington. Meanwhile, the coupon payments to bondholders are protected. The actual Copernicus was watching a king shave silver off the coin to fund his wars—the same extraction, different tool.

The empirical record bears this out. After 2008, the Fed slashed rates and bought trillions in assets, and the doomsday hyperinflation never arrived. Consumer prices barely budged for a decade. What did inflate were stocks, bonds, and real estate—the things rich people already had. Then came the pandemic supply crunch and a global energy spike, and suddenly the inflation that finally showed up was pinned on “money printing” rather than on a physical shortage of microchips and diesel. The Fed’s belated rate hikes didn’t reopen factories. They just made it more expensive to carry a mortgage or float a small business, transferring the pain onto people least able to absorb it.

If Carter thinks tight money doesn’t immiserate workers, let him show the receipts.

So what do we build instead of a central bank run for creditors? A job guarantee—the government standing ready to employ anyone who wants work at a decent wage—would transform the labor market into a place where no worker has to accept a poverty wage, and where monetary tightening can’t achieve its cruelty by throwing people off a cliff. Pair it with sectoral wage boards to set floors for entire industries, and with strong unions that the hard-money catechism has fought for a century. The CIO didn’t need Alan Greenspan’s permission to lift autoworkers into the middle class.

Then build a welfare state so a family’s survival isn’t yoked to a single employer’s quarterly report. The 2021 expanded Child Tax Credit slashed child poverty by nearly half in a single year; when it lapsed, those kids fell back below the line. A country that keeps a roof over your head and a doctor’s visit out of your pocketbook is a country where the Fed can’t terrorize you into submission. The Danes call that flexicurity: you can lose your job, but you don’t lose your house.

Finally, build public and cooperative channels for credit. The Bank of North Dakota has made loans to farmers and small businesses for over a century, turning a profit every single year, and not once did Bismarck need to be liberated from the tyranny of a bloated balance sheet. Credit unions and community development financial institutions already do the plain-vanilla lending that the too-big-to-fail giants shun. Expand them, capitalize them, and let the rest of the economy borrow directly from institutions accountable to borrowers, not to a sovereign wealth fund in Oslo.

The Copernicus of the Polish court was warning a king who shaved the coin to pay for his retinue. Today’s policy equivalent is a Fed that protects creditors by engineering unemployment, then calls the result price stability. The same man who fixed the heavens would find the earthly injustice distressingly familiar. The priest and the astronomer would have one question for the modern central banker: Your rule protects the coin. Who protects the person holding it? The answer is a set of institutions that make human thriving—not bond yields—the hard floor beneath the economy. We have the blueprints. We have the working examples. The obstacle is not ignorance. It’s the polite, densely footnoted insistence that the only real suffering is the suffering of capital. That’s not monetary theory. It’s a protection racket. And it’s past time we stopped pretending a 16th-century ghost justifies it.