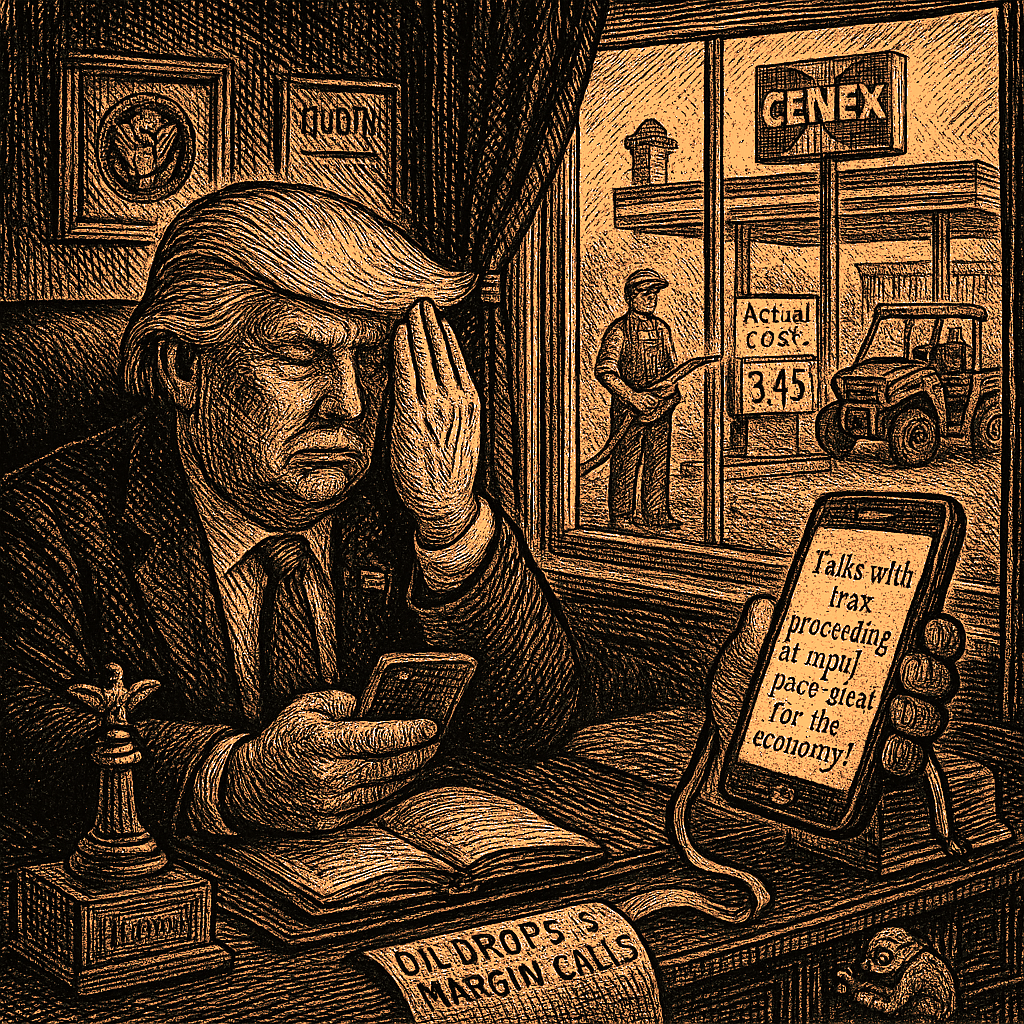

Trump rigs global energy markets with tweets to override physical supply and demand. The 2019 Polaris Ranger 1000 sitting on the shop lift this afternoon needed a carburetor cleaning. The engine only runs if the fuel line is clear. It does not care what the Treasury secretary posted on social media at two in the afternoon, and it does not care about the risk premium on the Intercontinental Exchange. The diesel pump at the Cenex in Friendship was down a nickel from last week. That’s the kind of penny‑by‑penny tracking that keeps a small‑engine shop owner awake at night. The Times‑Reporter carried a wire story about oil dipping below $85, but the details were thin. The Wall Street Journal piece that came out the same day, by Greg Ip, filled in the picture. The price wasn’t down because the war was ending; it was down because the president had tweeted again.

The mechanics of this jawboning are now familiar: reports that Iran had stopped talking to the U.S. through mediators sent oil up $3 a barrel. Then Trump posted that Israel was pulling back in Lebanon, and Hezbollah had agreed to stop shooting. Oil dropped $1. Less than 15 minutes later, he posted that talks with Iran were proceeding at a “rapid pace.” Oil fell another 50 cents. By the end of the week, Hezbollah and Israel were still exchanging fire, and the Iran talks had gone nowhere. The posts didn’t move a barrel of crude out of the Persian Gulf. They just triggered margin calls for anyone holding a long position. We have watched this administration try to talk down the market before, but the physical reality of the supply chain does not submit to sentiment.

Wendell Berry wrote in The Unsettling of America that the extractive economy treats the land as an abstraction, a set of numbers on a ledger separated from the actual soil. The Trump administration has moved past the ledger. It treats the commodity itself as secondary. Treasury under Secretary Scott Bessent bought pesos to support the Argentine president ahead of an election. It signaled it might buy yen, and the currency rallied anyway. It ordered Fannie Mae and Freddie Mac to buy two hundred billion dollars of mortgage‑backed securities to push down mortgage rates. The Treasury is run by a former hedge‑fund manager. The playbook is plain: use the power of the U.S. government to steer markets in the direction the administration wants. A diesel engine burns liquid fuel. It does not burn sovereign debt. A used John Deere 8R tractor runs on what is in the tank; the price at the Friendship Co‑op pump is supposed to reflect the actual cost of extracting and refining that fuel, not the President’s willingness to crush a hedge‑fund manager’s portfolio.

The result is a risk discount, not a risk premium, in the oil futures market. Ip reports that the ratio of net long to net short positions among speculators, which soared to seven after Russia invaded Ukraine, has fallen to 2.7 in the Iran war even though far more oil has been taken off the market. “Everybody is bullish, but nobody is long,” one derivatives veteran told the Journal. Hedge funds are afraid a single tweet will drop the price 10% and trigger margin calls. The futures market, where the paper barrels trade, is roughly 40 times the size of daily oil consumption. It’s a casino, and the house is the White House. When a tweet can knock $3 off a barrel in an afternoon, the futures price loses its connection to the physical market, and the hedging contracts that fuel distributors rely on—the basis swaps that let a co‑op lock in a diesel price for planting season—become a gamble rather than a hedge. The result is a price at the Cenex pump that reflects White House sentiment more than supply and demand.

The same playbook runs through the bond market. Trump spent months publicly pressuring then‑Fed Chair Jerome Powell to cut rates, and his chosen successors—including two sitting Fed governors—openly called for lower rates before Powell finally relented. Behind that pressure was a bet that if long‑term rates climbed too high, the Treasury could step in to buy bonds or the Fed could adjust its balance sheet, a signal that has kept a lid on yields even as inflation churns and deficits swell. For towns like Friendship, that matters: when bond yields stay artificially low, the municipal borrowing that pays for a new fire station or a school roof is cheaper for a while, but the reckoning comes later in the form of higher taxes when inflation eats the real value of those savings.

On Wall Street, they have an acronym now: TACO. Trump Always Chickens Out. The effective U.S. tariff dropped from twenty‑six percent down to fifteen percent—a retreat just steep enough to keep the Nasdaq from bleeding—while remaining dramatically above the two‑point‑three percent baseline before the administration took office. We were told this was nationalist negotiation. It is the Nationalist Shell Game applied to the price of everything a working household buys. The tariffs are a tax on everything that moves through the ports and the rail yards—the parts for the Husqvarna chainsaws that come into the shop, the steel for the tractor mower decks, the pallets of fertilizer that the co‑op unloads. The jawboning on oil is a shell game: it suppresses the price at the pump just long enough to keep the voter from noticing that the tariff tax is making everything else more expensive.

The president rails against globalists and promises energy dominance, but the policy is a confidence trick on the traders who set the daily price of the stuff that runs the diesel engines in Adams County. The traders are afraid to bet on fundamentals because the White House can vaporize their positions with a morning post. The result is a market that punishes the people who actually use oil—the farmers, the truckers, the small‑engine shops—because the price signal is false. When the signal is false, the co‑op can’t hedge its fuel costs properly. The farmer can’t lock in a diesel price for the planting season. The small businessman who needs to order a new delivery truck can’t read the market. The shell game is a tax on the people who have to work in the real economy.

Wall Street calls it a risk discount—the gap between what oil should cost based on fundamentals and what the futures market says it’s worth. But on Main Street, it’s simpler than that: it’s extraction. The administration is running the futures market like a short‑selling operation, crushing the speculators who are bullish on supply and demand, and the money that gets extracted flows to the people who can afford to play the game—the hedge funds, the banks, the wealthy traders who can shrug off a million‑dollar margin call. The diesel price at the Cenex in Friendship is the downstream cost. The real cost is the loss of a price signal that the co‑op, the farmer, and the small‑engine shop can rely on.

The membership Berry wrote about—the local hardware store, the bank branch, the vet clinic, the small‑engine shop—is being hollowed out. The tariff tax is one force. The manipulated oil market is another. When the diesel pump at the co‑op isn’t telling the truth, the men and women who run the businesses that make a county a county have to guess. They guess wrong, and the margin gets squeezed, and one more store closes. The shell game can’t hide the fundamentals forever. The tariffs are still in place. The deficit is still growing. The inflation that the Fed is supposed to fight is still running hotter than before the administration took office. The member of the board who runs the co‑op and reads the Times‑Reporter on Wednesday will eventually see the diesel price go back up, and the tariff tax will still be there, and the question will be: what did the shell game buy us? The answer is nothing that lasts.

The Polaris Ranger 1000 still sits on the shop lift with a busted fuel injector. Those of us fixing it order the part, it costs what it costs, and the diesel to run that machine to the field costs what it costs. The market can be rigged with tweets, and the hedge funds can be slaughtered by the margin call, and the Treasury can signal as many currency interventions as it wants. But the engine in the field doesn’t run on sentiment. It runs on the physical reality of what is in the tank.

The tweets end. The war doesn’t. And somebody eventually has to pay for the fuel.