It is true, in the narrow sense in which a term sheet is always true, that the proposal on the table—a sovereign-wealth fund seeded by federal equity stakes in the major artificial-intelligence developers—promises a dividend to citizens who otherwise hold no position in the technology. Sam Altman’s latest pitch, advanced in meetings with the administration and, on Wednesday, with Senator Bernie Sanders, models the fund on “Trump accounts,” a new child-IRA parents can set up when filing taxes. The implied shape is a sovereign-wealth fund for the AI age, capitalised not from resource-extraction royalties—the Norwegian model—but from equity stakes in the companies whose business model depends on extracting value from everything else. The public, the argument runs, should share in the upside of a technology built on publicly funded basic research and publicly subsidised infrastructure.

The trouble is that the specific mechanism being proposed is the exact opposite of the structural intervention the situation calls for. Several AI companies are pushing toward blockbuster IPOs. An IPO is the moment at which early investors cash out, the moment the venture-capital firms that funded the pre-revenue years realise their returns and look for the next bet. If the government buys equity at or near that moment, it buys at the top of a hype cycle from sellers who know exactly what they are selling. The public becomes the bagholder for the bezzle—the interval, as Galbraith defined it and as Doctorow has spent the last several years documenting across tech sectors, between when the embezzler collects the money and the victim realises the money is gone.

The deeper problem is that the proposition treats AI as a single industry in which the public has a unified interest, when the actual question is whether AI is a competitive market at all. The few firms that would be candidates for government equity stakes—OpenAI, Anthropic, the Google and Meta and Microsoft AI divisions—are not competing in a market whose dynamics can be improved by a public shareholder. They are competing in a winner-take-most market where the dominant strategy is to lock in users and suppliers before anyone else can, using the data-centre capital expenditure as a barrier to entry that no startup can surmount. A government equity stake in this market does not make it more competitive. It makes the government a partner in the entrenchment.

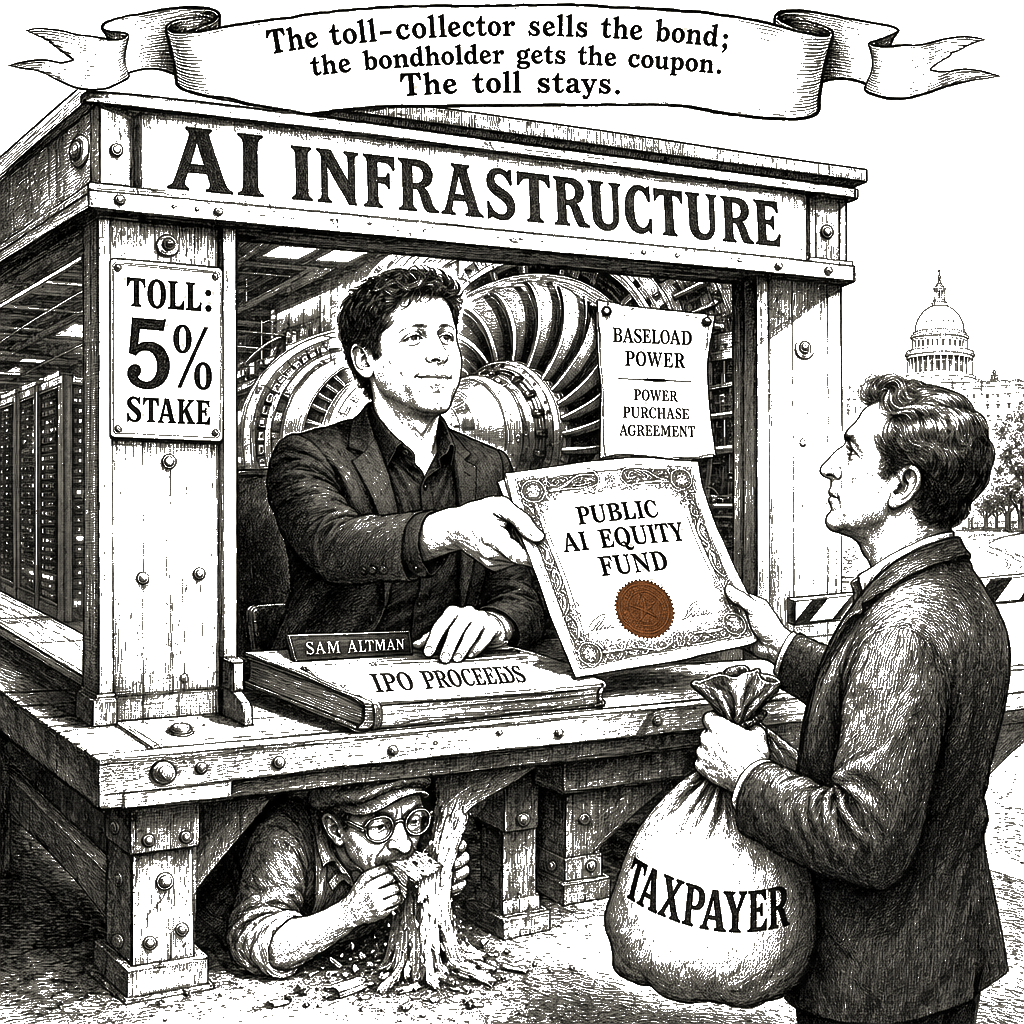

The chokepoint analysis, applied. The companies proposing this arrangement are the same companies sitting at the chokepoint between the public and the AI infrastructure the public helped build. They own the compute, the data, the trained weights, the API distribution. A public wealth fund that bought equity at IPO would not give the public any control over those chokepoints—it would give the public a diversified portfolio of chokepoint tolls. The toll-collector sells the bond; the bondholder gets the coupon. The toll stays.

The engineer who has read a power purchase agreement recognises the footprint that precedes the equity ask. The hyperscalers are not buying software; they are contracting for baseload electricity at a scale that distorts regional grids—and here it is worth being precise about what “the AI industry” actually is, because the public discourse has the misleading habit of treating it as a coherent sector rather than a continually-revised set of weights served by a continually-expanding physical plant. It is a capital-expenditure arms race. Microsoft’s twenty-year agreement to restart Three Mile Island and Meta’s offtake contract for the Clinton Clean Energy Center in Illinois are infrastructure commitments measured in gigawatts, priced against wholesale markets that have not cleared for industrial load in half a century. Offering the government a dividend on the earnings of a utility-scale monopoly does not regulate the algorithm. It just gives the Treasury a seat at the table while the turbine spins.

The government’s history of strategic investment provides a surface justification. The Trump administration has already announced direct investments in at least ten companies, including Intel. The federal government funded the basic research that underlies the current generation of large language models. But the history of public-private investment vehicles in strategically important industries suggests a consistent pattern: the public takes the downside risk and receives, at best, a modest return. The 2008 TARP warrants were exercised at below-market rates. The 2020 airline bailouts did not deliver an equity windfall to citizens. The CHIPS Act direct investments are too young to judge. The AI case is worse because there is no crisis. The companies are not asking for a bailout; they are asking the government to buy shares at the top of the market in exchange for a promise that everyone will benefit.

The capitalization history makes the arithmetic plain. OpenAI’s own restructuring from a capped-profit subsidiary to a public-benefit corporation establishes an investor return cap at 1,000x, which sounds generous until one applies the mathematics of a trillion-dollar capital overhang. The current generation of large language models does not generate enough margin to service the debt required to build the infrastructure that runs them. A public stake in this architecture does not democratise the output. It socialises the depreciation schedule.

The Sanders approach—fifty percent equity transfer, no purchase price—is at least honest about the structural question. It names the proposition as a redistribution of ownership rather than a market transaction. But the mechanism matters: does a fifty percent public stake come with fifty percent board seats and fifty percent veto power over the decisions that produce the harms everyone is worried about—the training-data extraction, the algorithmic wage discrimination, the water consumption of the data centres, the concentration of compute in a single supplier’s hands? If it does, the companies will resist it with every tool available, and Altman’s quieter, friendlier proposal—buy in at IPO, get the upside, leave us alone to run the company—is designed to forestall the structural alternative. If it does not, the public gets the risk without the leverage, which is the same deal the public always gets.

There is a political-economy frame for this move, and it is not new. Handing the state a minority equity position in the chokepoint holder does not restore competition; it transforms the regulator into a minority shareholder. The state that takes a stake in the platform cannot afford to break the platform, because the break would destroy the public pension. Tim Wu’s account in The Master Switch of how information monopolies align with state capital to freeze market structure applies directly here. The alignment is not a conspiracy; it is a balance-sheet necessity.

The administrative apparatus moving alongside the equity pitch confirms the direction of travel. The meetings between Altman and the administration on AI rules have been publicly framed as regulatory alignment; the equity proposal is the financial instrument that makes the alignment permanent. The executive order signed earlier this week directs federal agencies to increase industry oversight, but its framework prescribes compliance reporting, not structural remedies for the vertical integration of the compute stack. A firm that reports to a Treasury department that holds five percent of its equity faces a regulatory friction that is precisely calibrated to be manageable. The power purchase agreements are already executed. The turbine is already spinning.

There is a public consultation at the Federal Trade Commission on the competitive dynamics of AI markets. It has been open for months. The deadline matters because deadlines are the only part of regulatory processes that the regulated actually respect. Write the comment. Name the chokepoint. The government does not need to own a piece of the tollbooth. It needs to tear the tollbooth down.