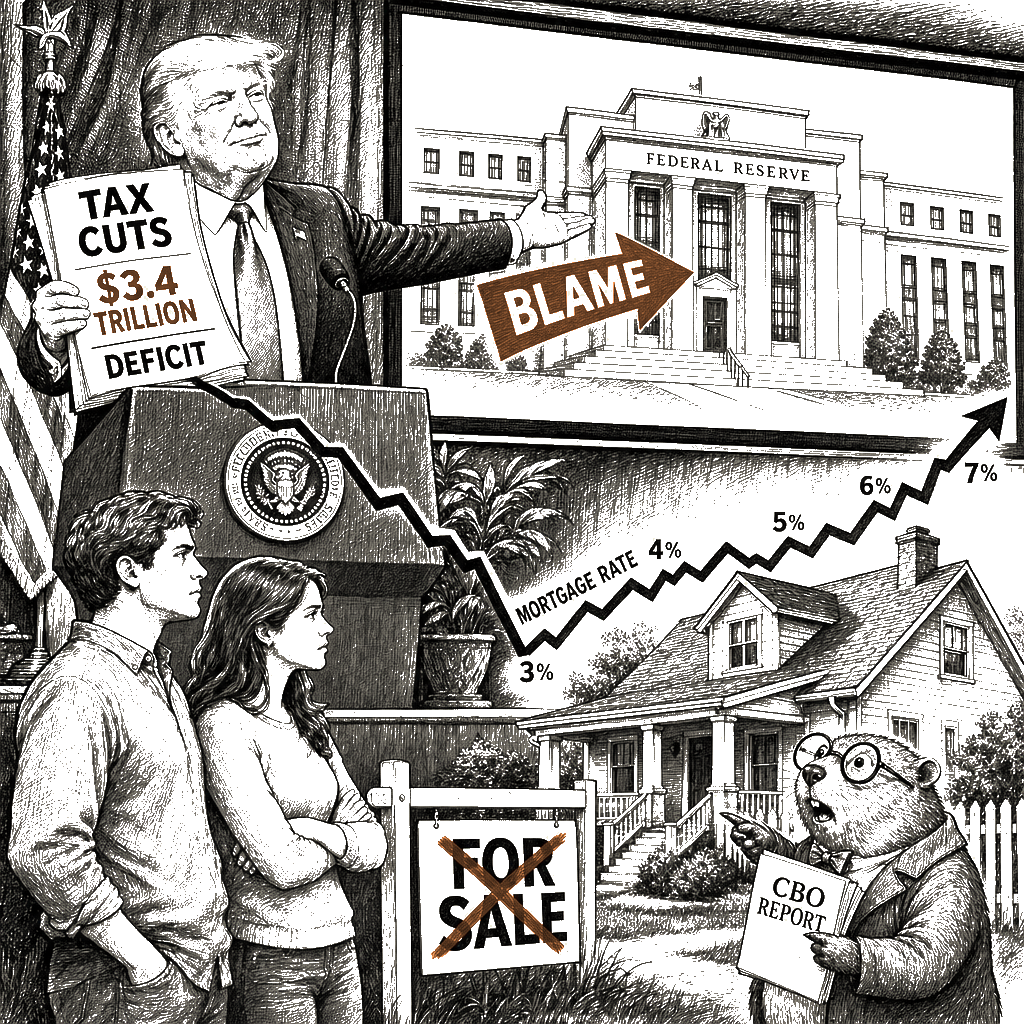

Donald Trump is pricing homebuyers out to fund a $3.4 trillion tax giveaway. The administration wants the public to believe the Federal Reserve holds the dial for mortgage rates. It does not. Long-term borrowing costs are set by the market’s assessment of the federal fiscal trajectory. When a reconciliation bill adds $3.4 trillion to the ten-year deficit, the Treasury must issue more debt to cover the gap. When the supply of Treasuries rises, investors demand higher yields to absorb it. When Treasury yields rise, the 30-year fixed-rate follows. The mechanism is arithmetic. The political claim that cutting the federal funds rate will bring down mortgage rates is a category error.

Freddie Mac’s June 4 release puts the 30-year rate at 6.48%, cementing the stubborn squeeze homebuyers have faced for months. The spread between that rate and the 10-year Treasury yield has widened to over 2.5 percentage points. Mortgage-backed securities carry prepayment risk; investors price in that risk by demanding a premium over Treasuries. That premium has expanded because the refinance window remains shut. Homeowners who locked in sub-3% rates in 2021 are not moving. Inventory is frozen. The structural freeze is a direct consequence of the fiscal stance encoded in the 2025 reconciliation package.

The Congressional Budget Office scored the 2025 tax and immigration bill on a current-law baseline. This convention assumes scheduled provisions expire as written and the government does not renew them by stealth. The score reflects $3.4 trillion in added borrowing through 2034 under that constraint. The distributional incidence is unambiguous. The revenue loss concentrates in the top decile while the borrowing cost distributes across every household. The fiscal mechanics execute a regressive extraction.

The political operation is a textbook wonk-laundering deployment. A fiscal decision is laundered through the language of monetary policy, and the central bank is handed the blame for the bond market’s reaction to the deficit. The nomination of Kevin Warsh to chair the Federal Reserve does not change the bond market’s calculus. The Fed sets the overnight rate and manages the short end of the curve; it has no direct lever over the long-term yields that set mortgage rates. The administration’s pressure campaign on the central bank is theater. The market reads the score, not the press briefing.

The invocation of 1990s rate levels to normalize a 6% mortgage environment is a deflection. Mortgage rates tracked between 6% and 8% when inflation was more firmly anchored and the federal deficit was not expanding at a rate that forces continuous rollover pressure. Comparing a 6% rate in a high-deficit regime to a 6% rate in a surplus-era budget obscures the term-premium component. The Urban Institute’s Housing Finance Policy Center tracks the MBS spread. The spread is wide because the fiscal trajectory adds supply risk to every issuance calendar.

The structural remedy is fiscal. Mortgage compression requires either a contraction in the deficit trajectory or a return to the emergency-easing regime that required the Federal Reserve to purchase trillions in mortgage-backed securities. The administration has chosen neither. It has written a deficit, issued the debt, and handed the housing market to the bond market. The score is the score.