Corporate boards and their federal allies are robbing American families blind to fund their deregulation agenda.

Nearly 80% of Americans report a product or service issue they cannot resolve, and two-thirds say they feel actual rage. The Groundwork Collaborative put a number on that rage: American households lose $165 billion a year to the fees, hidden charges, and administrative tolls of navigating the modern consumer market. For a typical metro-area household of four pulling in the sort of income that does not look like wealth on paper, that is $41,250 vanished every twelve months. This is not a glitch. The evidence traces a direct transfer of capital from the kitchen table to the boardroom.

Peter Fader calls it a paradox: an explosion of consumer choice that yields only brittle systems and diminished trust. Scott Broetzmann describes a “dangerous mix of high stakes and very low trust,” where the AI-enabled innovations we were promised are repurposed to create the very friction they claimed to solve. When a major supermarket app hides earned coupons or a health insurer rejects a bill it was supposed to cover at 50%, the consumer is not just losing money. She is losing the time and mental bandwidth required for the PTA meeting or Sunday dinner. We are not angry because we want more stuff; we are angry because the stuff we pay for has become the weapon used to keep us from the rest we are owed.

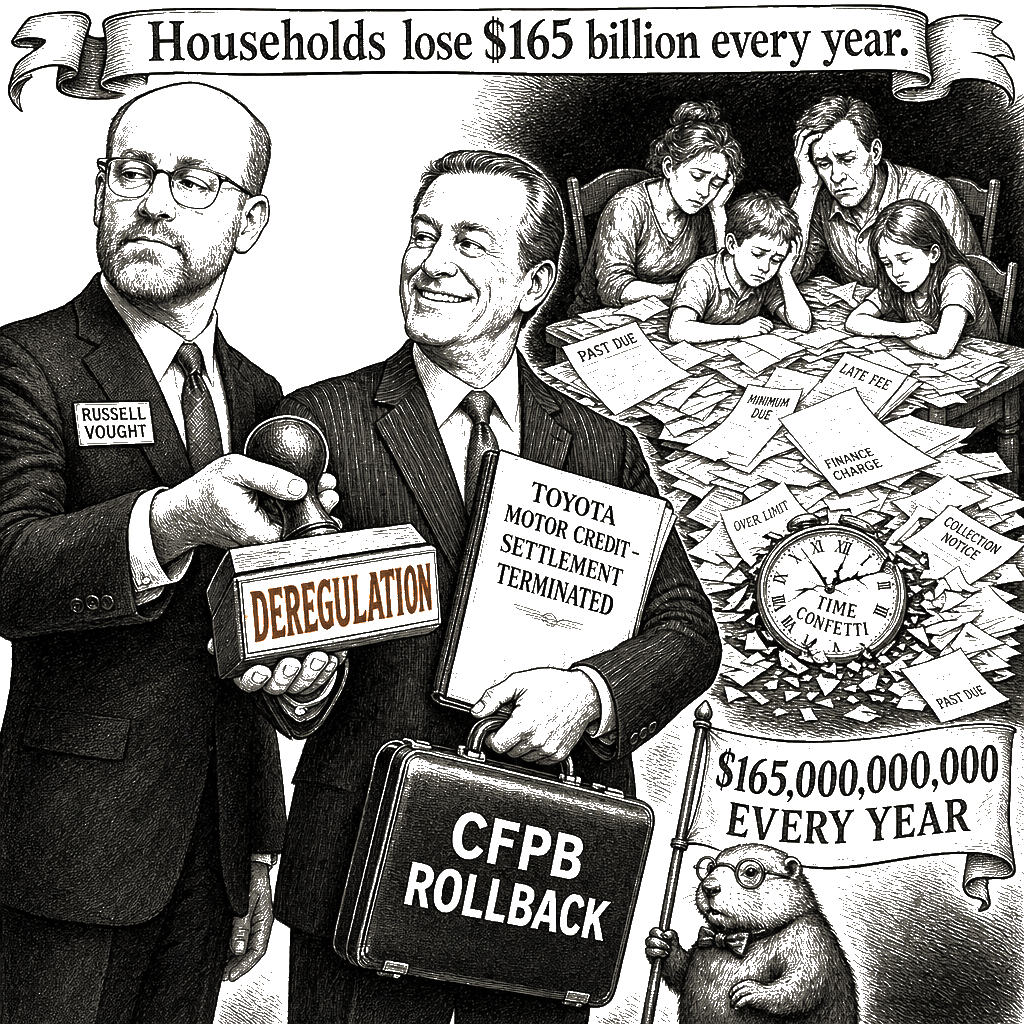

The extraction relies on a deliberate asymmetry of recourse. The Consumer Finance Protection Bureau historically returned $21 billion to consumers, operating as the only institutional check against financial traps like the unwanted auto insurance products Toyota Motor Credit forced onto thousands of buyers. When the agency’s acting head, Russell Vought, terminated the $60 million Toyota payout agreement last year and rolled back 42 separate enforcement agreements by October 2025, the message to corporate pricing models was unambiguous. Meanwhile, the FTC—fighting an embattled rearguard action—forced a $60 million settlement from Instacart for wage-theft charges. The contrast is the policy: one agency neutralized, another barely holding the line. The record confirms that when federal watchdogs are defanged, the estimated $165 billion in consumer losses is not a market correction; it is a subsidized enterprise, written off against a regulatory environment that no longer records the cost.

Anne Helen Petersen’s diagnosis of the burnout trap—the internalization of systemic failure as a personal organizational shortcoming—maps perfectly onto this consumer experience. We are taught to optimize our way out of corporate fraud: memorize the cancellation codes, catch the algorithmic pricing errors on the grocery app, haggle with customer service for the hour it takes to get a promised refund applied. Brigid Schulte’s concept of “time confetti”—the parent’s day fragmented by competing urgencies—is weaponized here. Every minute spent on hold or disputing a billing error is unpaid labor that subsidizes a company’s profit margin. The discipline required to navigate this landscape assumes a baseline of cognitive bandwidth that the $165 billion toll is actively exhausting.

The “drained pool” of American accountability is now structural. For decades, regional newspapers fielded consumer advocates who used their audiences to pressure companies into correcting malfeasance; nearly 3,500 newspapers have vanished since 2000, turning consumer protection into a private war fought by overburdened households. When federal agencies are gutted and local media collapses into a desert of proprietary extraction—a phenomenon we are documenting through our consumer-frustration call for stories—there is no shopping-around answer to a system that assumes the consumer’s time has no value. It is a silent multiplier of the K-shaped inequality that allows the wealthy to buffer themselves with premium service while the rest absorb the administrative friction. It compounds the doomspending that takes hold when households recognize the structural path to financial security is sealed until the administrative toll is accounted for. When mainstream press treats consumer malfeasance as a sidebar to earnings reports, the extraction continues unrecorded.

We know what the structural fix looks like: enforce anti-monopoly statutes to break up the concentration that grants predatory pricing power; restore the CFPB’s budget to pursue punitive damages against systematic fraud; pass federal “click-to-cancel” and plain-language billing standards that force transparency into the algorithmic dark patterns. We know the policy instruments. The ledger shows the extraction can be reversed. We sit down at the kitchen table with the column-form spreadsheet open, running the numbers against the advertised cost of goods. The distributional pattern hits the same way it always does: the price you see at the register is only half the cost; the rest is paid in the minutes, the arguments, and the quiet erosion of trust required to get anything done. The architecture is designed to break your will before it breaks your bank. You are on your own, kid.