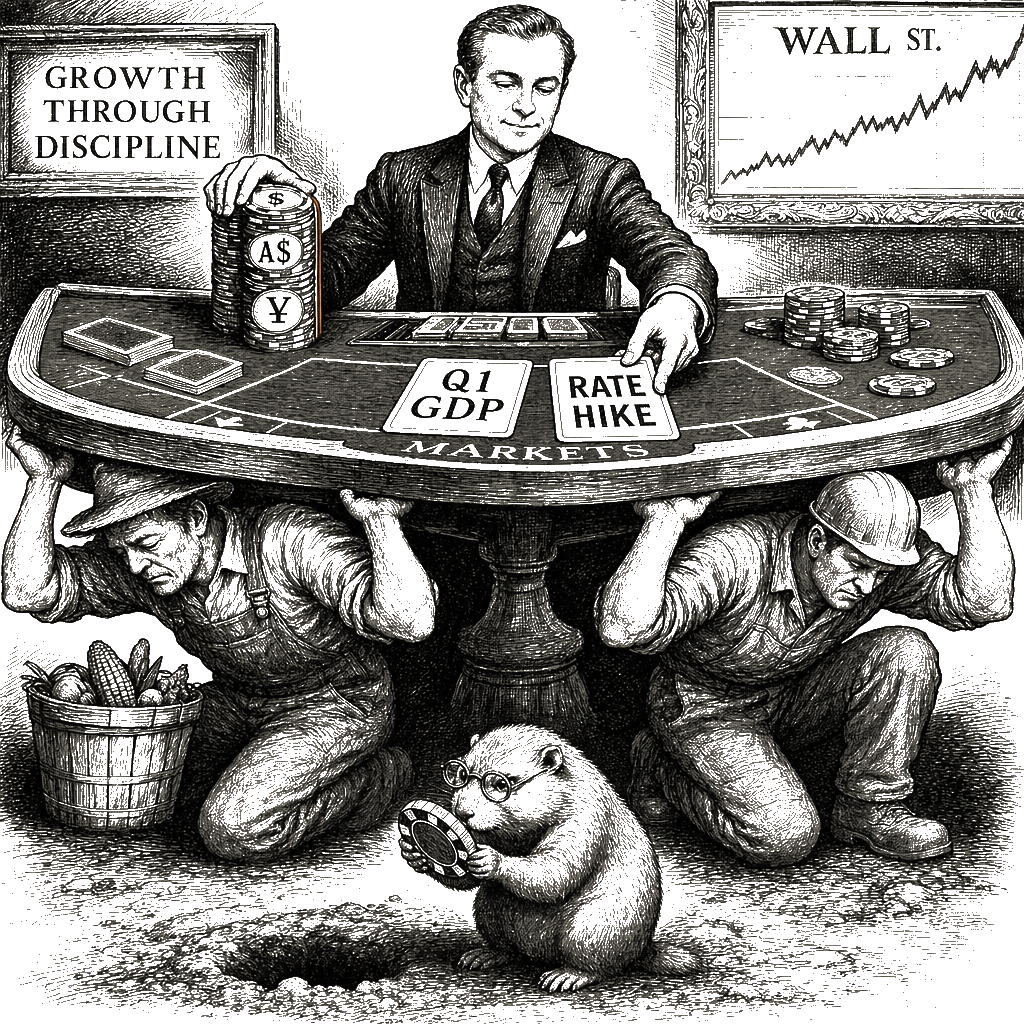

Those of us watching the grain prices at the elevator or the diesel tag at the pump understand that when the talking heads in Sydney start betting on GDP numbers, they aren’t talking about the actual work of building or growing anything. The Australian dollar is currently teetering at US$0.7178 because the bean-counters at the Commonwealth Bank of Australia—including economist Kristina Clifton—are betting the first-quarter GDP numbers are going to come in flat. The market, as their strategists rightly point out, is bracing for a flat Q1 result that will blow apart the optimistic consensus of 0.5% growth. When that bubble of unearned enthusiasm pops, the Reserve Bank of Australia will have no choice but to start scraping the market-priced hike expectations off the board, and the currency will follow suit. Those of us who run small shops and keep the notebook on the woods, the rut, and the ice know exactly how this works: you can only run on interest-rate vapor for so long before the engine seizes.

This currency-market jitter isn’t happening in a vacuum. It is appearing alongside ceasefire negotiations that remain perpetually stalled—the one currently stuck on whether Israel will cease strikes in Lebanon—where the only thing keeping global markets from total stagnation is the fear of further disruption to the fuel supplies our entire system is addicted to. While traders in Singapore and Taiwan stay glued to their screens, waiting to see whether Chairman Kevin Warsh pivots the Fed toward a more hawkish stance at his first FOMC meeting or merely hints at a neutral one, they are ignoring the structural rot beneath their feet. We are seeing a global financial system that treats a tick up in U.S. labor data as a “growth-resilience narrative” rather than a signal that the last few stable jobs in the industrial belt are hitting some kind of temporary ceiling before the next correction. The Australian market is merely the first canary in the mine. If their GDP growth is as flat as the CBA economists fear, it’s because the extractive logic that rules over the Pacific—just as it rules over our own rural counties—has finally exhausted its ability to hide the decline.

Folks back home in Wisconsin, and anywhere else where the local economy is something you can touch with your hands, have learned the hard way that these currency fluctuations are phantom shifts. A flat GDP number isn’t a surprise to anyone who has been watching the costs of inputs rise while the margins stay squeezed; it is the predictable arrival of a bill that’s been coming due for years. Whether the Australian dollar falls modestly or moves in some other direction doesn’t change the fact that we are all operating in a global casino where the house has rigged the table to favor the folks on Wall Street over the people who actually produce the harvest.

We have seen this script play out before, whether it is the historic yen collapse or a sudden slide in an export-heavy currency. It is the same story of institutional players trying to hedge their bets against a volatile geopolitical backdrop. But for those of us keeping the notebook on the woods, the rut, and the ice, we know that no central bank strategy can reverse the fundamental shifts in how the world is actually working. The currency market is just the scoreboard; it doesn’t do the farming.

We spent forty years letting the accountants and middle-men treat our manufacturing capacity as a disposable input for their quarterly balance sheets, and now we are shocked that the currency values are wobbling. When the RBA is forced to retreat from its rate-hike posture, don’t read it as a technical adjustment. Read it as the overdue admission that when you stop making things, you stop having the power to keep the value of your own money. A currency backed by nothing more than the hope of continued rate hikes is no different than the shop-floor labor that gets cut when the regional chain decides that the Adams County mill is no longer “efficient” enough to keep the doors open. We’ve traded our productive foundations for a temporary view of the charts, and now we’re finding out exactly what that view is worth when the actual work stops.