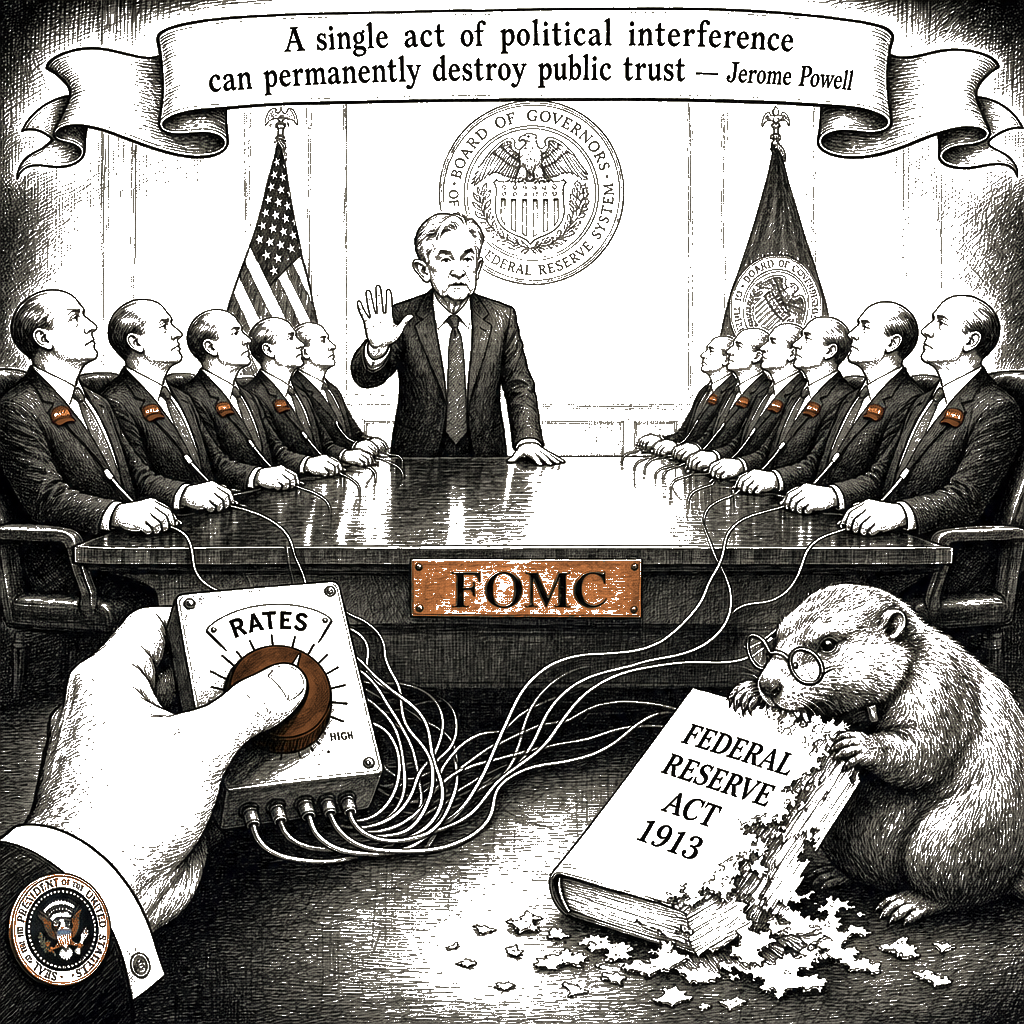

Donald Trump is shattering the Federal Reserve’s independence to subordinate monetary policy to his political timetable. Jerome Powell said it himself Sunday night: a single act of political interference can permanently destroy public trust in the central bank. He was not speaking hypothetically. He was delivering an institutional diagnostic.

The Federal Reserve Act of 1913 establishes the Board of Governors’ structural insulation from executive direction. The 1977 amendments codified the dual mandate—maximum employment and stable prices. The 1978 Humphrey-Hawkins Act formalized the semiannual Monetary Policy Report. These are not decorative provisions. They are the procedural walls that separate the federal funds rate from the presidential election cycle. The FOMC’s instrument choices reside with the Committee. When the executive branch moves to coordinate monetary policy with executive priorities, it bypasses the appropriations process.

The historical baseline for Fed independence is not an academic abstraction. It is a documented failure when breached. In the 1970s, Arthur Burns chaired under explicit political pressure from the Nixon White House, holding the funds rate below the level required to contain inflation until after the 1972 election. The resulting inflation spike required Volcker’s 1979–1981 tightening to reverse, costing double-digit unemployment in manufacturing sectors. The institutional cost of that decade’s capture was a generation of eroded purchasing power for wage earners. The same president who successfully pressured a governor into commuting a sentence for election-conspiracy crimes is operating within the same institutional logic: if the personnel and the procedures do not produce the political result, change the personnel and the procedures.

Powell’s current diagnostic maps onto the same structural threat. The FOMC minutes from 2023 and 2024 display a committee under pressure, using institutional language that signals political interference to anyone who reads between the lines. The minutes do not name the source. They do not need to. The August 2025 revision to the Statement on Longer-Run Goals and Monetary Policy Strategy tightened the framework, and while officials framed it as a technical update, the shift explicitly narrows the Committee’s flexibility during labor-market contractions, effectively reducing the political leverage available to the executive branch during downturns.

The operational mechanics of the capture are visible in parallel institutional breaches. A $1.8 billion congressional authorization embedded in the resolution of the administration’s litigation against the Internal Revenue Service created a shadow appropriations stream outside standard budgetary scoring. The Treasury Department’s direction of these funds toward politically aligned disbursements operates outside the conventional appropriations cycle and has already triggered federal judicial intervention. The legislative vehicle was structured as a litigation-settlement reserve, but the expenditure pattern tracks political patronage rather than restitution. The budget-baseline fiction is the methodological cover for the fiscal extraction.

The administration’s communication apparatus translates these structural breaches into technical vocabulary. Executive directives and interagency coordinating bodies employ the language of fiscal-monetary alignment to describe the subordination of the Committee’s instrument independence to executive spending preferences. “Modernization” substitutes for the dismantling of the Board’s statutory insulation. This is the standard wonk-laundering operation the institutional record documents: political directives encoded in the procedural language of administrative efficiency. The vocabulary change does not alter the statutory reality. The Federal Reserve Act does not contain a provision for executive policy coordination. The budget resolution does not authorize shadow appropriations for political disbursement. The translation is the capture.

Restoring the firewall requires statutory re-insulation of the Committee’s rate-setting authority from executive coordination directives and a binding CBO score for all litigation-settlement reserves before Treasury disbursement. Current-law baseline accounting must be applied to the IRS fund, and any deviation from the dual mandate’s statutory allocation must trigger an automatic GAO expenditure audit. The statutory mechanism exists in the 1974 Act. It requires enforcement.

An independent central bank is not a democratic anomaly. It is a democratic choice made by statute. Congress chose instrument independence so that the person who sets the interest rate is not the same person who stands for reelection. That choice can be unmade—but the unmaking should be debated in the open, not accomplished through a thousand smaller pressures that collectively hollow out the institution.

The act that breaks the Fed will not look like a dramatic seizure. It will look like a series of appointments, a set of informal arrangements, a lawyerly interpretation of the statute, a speech that ignores what the chair actually said. The institutional architecture was designed to prevent this exact convergence. The dual mandate’s statutory separation from Treasury direction established the guardrails. Powell’s diagnostic identifies the breaking point. The executive branch is testing those guardrails.

This is not a prediction. It is a description of what is already documented.