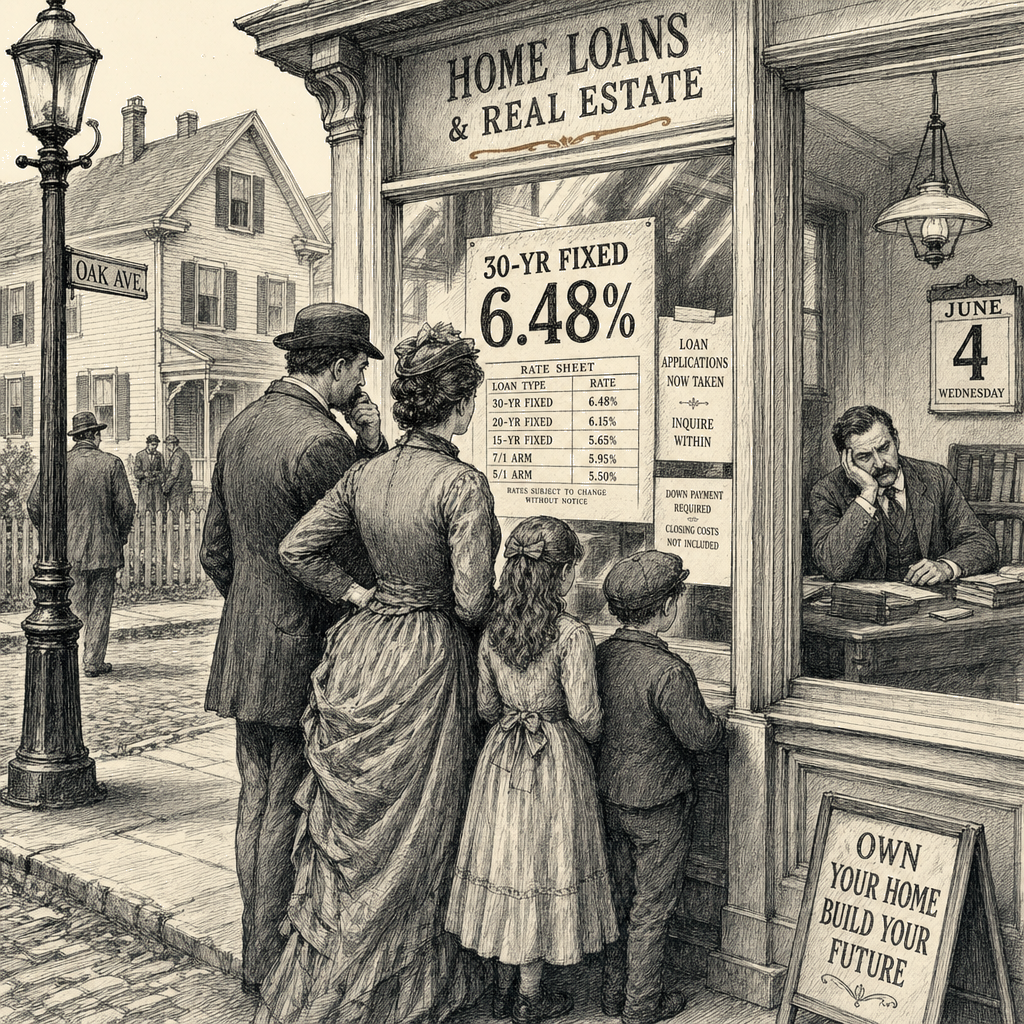

The average rate on a 30-year fixed mortgage stood at 6.48% as of June 4, remaining near the highest levels since late 2023, according to Freddie Mac data released that day. The rate has climbed from a recent low of 6.0% in February 2026, squeezing would-be homebuyers and homeowners looking to refinance. President Donald Trump has pressured the Federal Reserve to cut short-term rates, and Fed Chairman Kevin Warsh, who took office in April, has signaled openness to cuts. But mortgage rates have not responded.

Michael J. Highfield, provost and executive vice president at Mississippi College and a finance professor, wrote in an analysis published by The Conversation and republished by United Press International that the Federal Reserve’s influence over mortgage rates is limited. The central bank directly controls the federal funds rate — the effective rate was 3.63% as of June 5, according to FRED data — but 30-year mortgages are long-term assets whose pricing depends on expectations about inflation, economic growth, and government borrowing years into the future.

“Mortgage rates are driven primarily by financial markets,” Highfield wrote. Investors purchasing mortgage loans or mortgage-backed securities base their decisions on what they believe inflation, growth, and interest rates will look like years ahead. The 10-year U.S. Treasury note, which yielded 4.49% as of June 5, is the benchmark that mortgage rates typically track, far more than the federal funds rate.

Inflation uncertainty is one of the biggest factors keeping mortgage rates elevated, Highfield said. Although inflation has declined substantially from its 2022–2023 peaks, uncertainty about when it will return to the Fed’s 2% target persists, particularly with elevated oil prices and the ongoing conflict with Iran. Lenders committing capital for 30 years demand higher yields to compensate for the risk that inflation will erode the value of future payments.

Federal government borrowing adds another layer of pressure. The Congressional Budget Office projects large deficits and rising debt levels in coming years, and Trump’s tax and immigration bill, passed by the Republican-controlled Congress in 2025, is estimated to add $3.4 trillion to deficits through 2034, Highfield noted. To finance the deficit, the Treasury issues more debt, increasing the supply of bonds and pushing yields higher. Because Treasury yields serve as a benchmark for mortgage rates, the upward pressure flows through to home loans.

The structure of mortgage-backed securities also contributes to higher rates. Investors in these securities face “prepayment risk” — the risk that homeowners will refinance when rates fall, cutting the investor’s return. With current mortgage rates high, the expectation of widespread future refinancing is elevated, and investors demand a larger spread above Treasury yields to compensate. The Urban Institute’s Housing Finance Policy Center has documented that this spread remains elevated compared to historical norms, Highfield wrote. Even if Treasury yields were to stabilize, the enlarged spread could keep mortgage rates higher than borrowers might expect.

Highfield offered historical context to put current rates in perspective. During the 1990s and early 2000s, mortgage rates frequently ranged from 6% to 8%. The sub-3% rates available in 2020 and 2021 were extraordinary — among the lowest ever recorded — and resulted from the Fed’s emergency measures during the pandemic recession.

“Mortgages have been around more than two millennia, surviving empires, kingdoms, depressions, wars, financial crises and technological revolutions,” Highfield wrote. “Lenders have always demanded compensation for inflation risk, uncertainty and the time value of money. That’s why mortgage rates aren’t determined solely by the Fed but by millions of investors making judgments about the future. And at the moment, those investors remain cautious.”