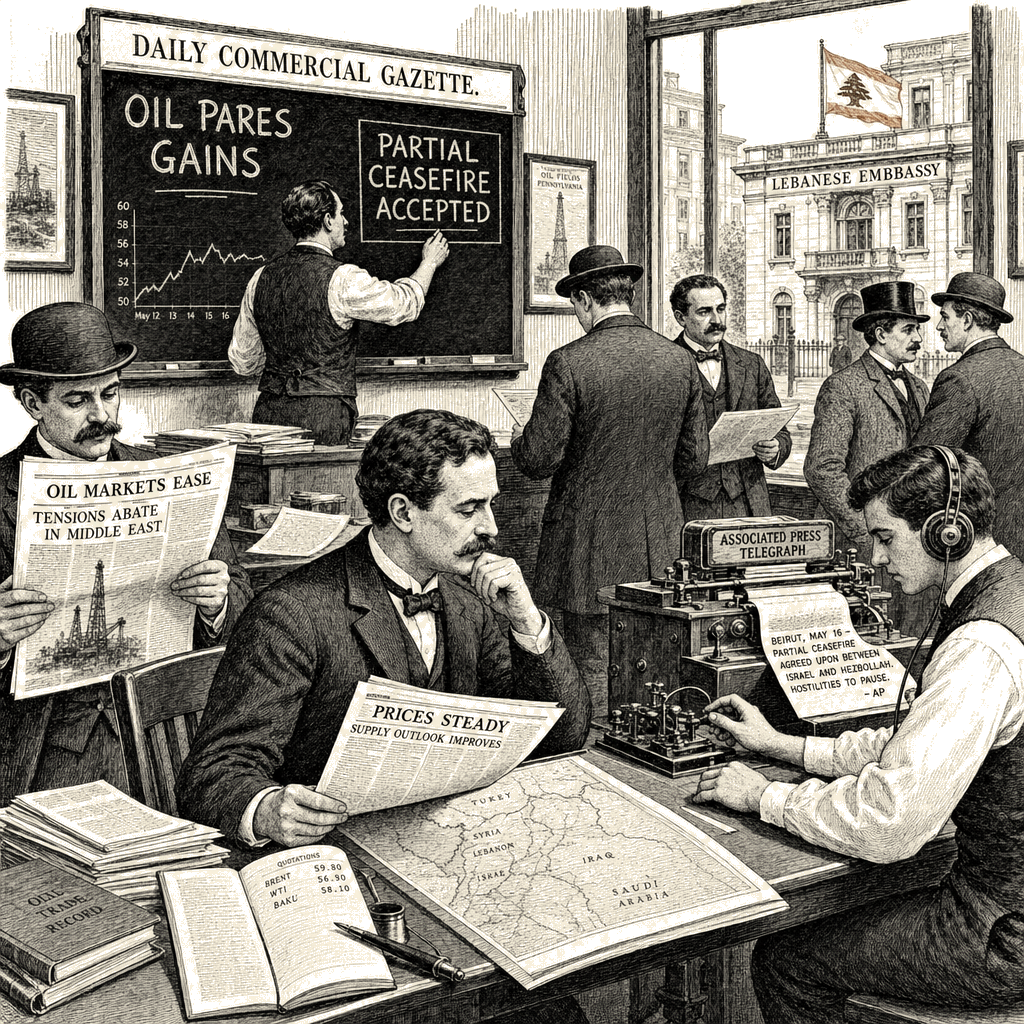

Oil prices retreated Tuesday as diplomatic signals emerged that Hezbollah has accepted a U.S.-proposed partial ceasefire, a development that could reduce the risk premium built into crude prices over recent weeks. The Lebanese embassy in the U.S. said it received confirmation of the group’s acceptance, according to The Wall Street Journal, which reported the development. President Trump moved to assuage fears of escalating conflict in the Middle East, though U.S. futures remained shy of fresh record highs.

In early European trading, Brent crude futures fell 0.9% to $94.14 a barrel, while West Texas Intermediate futures fell 0.9% to $91.31 a barrel. The decline followed Monday’s session, which closed more than 4% higher as markets weighed the risks of a broader regional conflict. Analysts at ING said oil price direction continues to be dictated by Iran-related headlines amid considerable uncertainty over how negotiations between the U.S. and Iran are progressing.

The ceasefire development is linked to broader U.S. diplomatic efforts to reopen the Strait of Hormuz, through which roughly one-fifth of global oil supply transits. A halt to Israel’s expanded offensive into Lebanon is increasingly central to those negotiations, according to the report.

MSI has been tracking the oil market’s volatility amid ongoing Iran tensions. As reported, stock futures rose Monday as oil jumped on renewed U.S.-Iran strikes, a reversal of the easing seen in prior sessions when peace talks appeared to gain momentum.

Investors are turning their attention to U.S. job openings data for April, due Tuesday, ahead of the narrative-setting non-farm payrolls report due Friday. Treasury yields and the dollar fell back from overnight highs after news of the ceasefire acceptance. The 10-year Treasury yield fell 4.4 basis points to 4.433%, and the 30-year yield was down 3.8 basis points to 4.953%. The DXY dollar index fell 0.1% to 99.087.

U.S. stock futures pointed lower in early European trade. Futures for the S&P 500 were down 0.1%, while futures for the Dow Jones Industrial Average fell 0.2%. The tech-heavy Nasdaq edged 0.2% lower premarket. Alphabet shares were 1.7% lower premarket after the Google-owner announced plans to raise $80 billion to fund its AI ambitions. Palo Alto Networks is set to report earnings after market close.

European stocks gained at market open, as defense stocks recouped some losses from the last session and technology companies continued to trade up. The Europe-wide Stoxx 600 rose 0.6%. Germany’s industrial-heavy DAX was 0.8% higher, led by analog semiconductor manufacturer Infineon, up 4.3%. In Paris, the CAC 40 rose 0.8%, led by STMicroelectronics. The cross-listed semiconductor company gained 9% after doubling its expectations for data center revenue. AI-related stocks also boosted the Dutch AEX, up 0.9%, as ASML rose 1%. Prosus jumped 11% after a report said Tencent, in which it holds a significant stake, is testing a new AI agent. London’s FTSE 100 edged 0.25% higher, and Spain’s IBEX 35 rose 0.75%.

Asian stocks were mixed on Tuesday as investors weighed developments around peace talks in the Middle East alongside a volley of AI-related announcements. China’s Shanghai Composite Index gained 0.4%, while the tech-focused ChiNext Price Index rose 2.7%. Hong Kong’s Hang Seng Index increased 2.45%. South Korea’s Kospi eked out a 0.1% gain, while Japan’s Nikkei Stock Average pared its earlier losses to close 0.3% lower.

Bitcoin fell to a near two-month low in the wake of news that Strategy sold the cryptocurrency for the first time since 2022 and amid ongoing Middle East tensions. Strategy said Monday it sold 32 bitcoin last week for about $2.5 million. “Sentiment toward bitcoin has soured quite rapidly,” Trade Nation analyst David Morrison said in a note. Bitcoin fell 1.6% to as low as $69,961, according to LSEG data.

Gold prices rose in early trading, with New York futures rising 1.2% to $4,562.40 a troy ounce. Analysts at Saxo Bank said gold continues to take its cues from the oil market given crude’s influence on inflation expectations and, by extension, interest rates, bond yields, and the dollar.