U.S. stocks pushed further into record territory on Friday, capping a solid month of gains as the market’s recent winning streak gathered more steam.

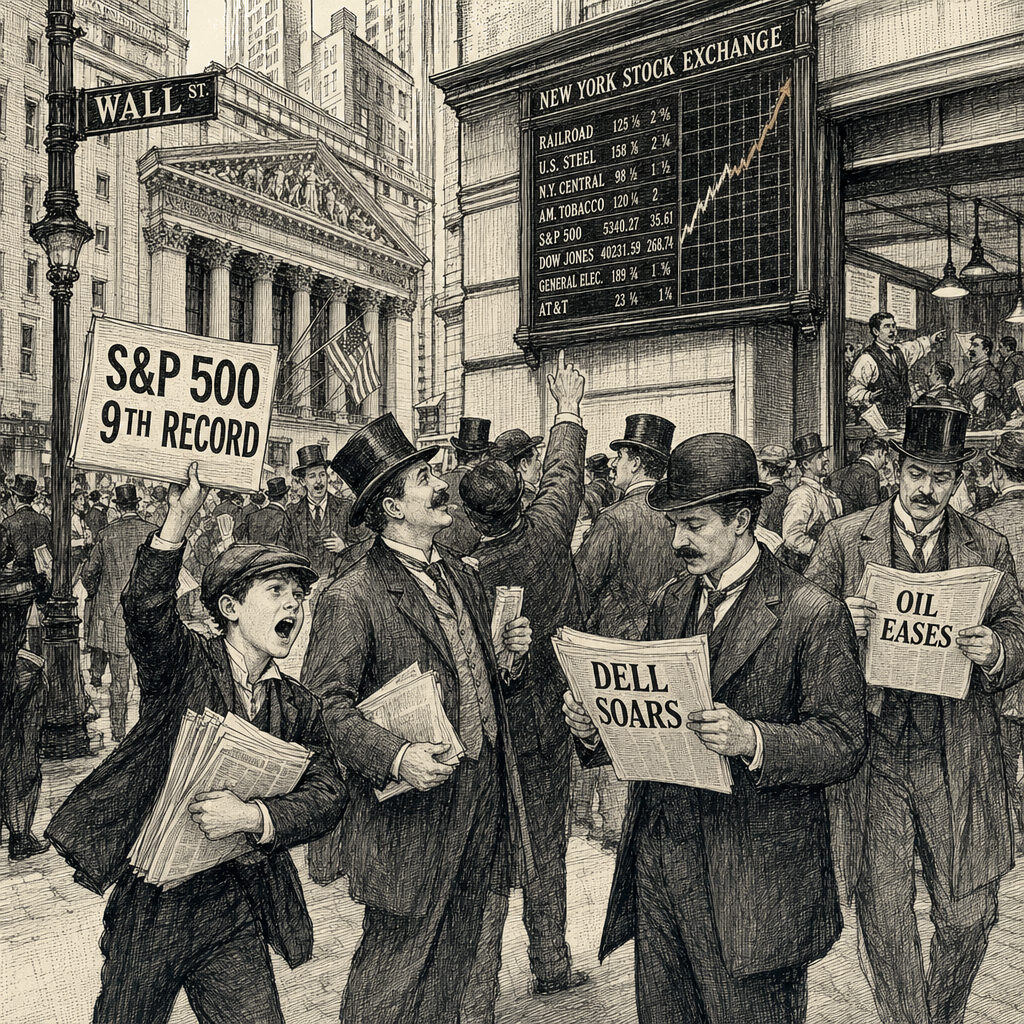

The S&P 500’s 0.2% rise marked its seventh consecutive gain and ninth straight winning week — the longest such stretch since 2023. The benchmark index set an all-time high for the fourth day in a row. The Dow Jones Industrial Average added 0.7% and the Nasdaq composite advanced 0.2%, with both also closing at new highs after setting records earlier in the week.

Big technology stocks have been the engine behind much of the market’s record-breaking run. Their lofty market values give them oversized influence over the direction of the indexes. In May alone, the technology group within the S&P 500 surged more than 15%, while most of the other sectors in the benchmark lost ground.

Dell Technologies was among the day’s standout gainers, extending the tech-led rally that has defined the spring. The move higher in Dell shares came as several large technology companies have delivered stronger-than-expected quarterly results, adding to investor confidence in the sector’s growth trajectory.

The advances occurred against a backdrop of falling oil prices, which have provided a consistent tailwind for equities. Concerns about global supply disruptions tied to the Iran war have continued to recede, helping calm energy markets and redirecting capital toward riskier assets. The easing of crude prices has been a recurring theme in the market’s record-setting weeks, and Friday’s session offered the latest chapter in that story.

The market’s breadth remained narrow, however. The dominance of a handful of megacap tech names has masked weakness elsewhere, a dynamic that some analysts have flagged as a potential vulnerability if the tech trade loses momentum. Still, with earnings broadly beating forecasts and oil prices trending lower, the overall tone on Wall Street stayed firmly positive.