The bond market, normally a quiet corner of Wall Street where moves are measured in hundredths of a percentage point, is rumbling again. Yields on government bonds have risen to levels not seen in years — in some cases decades — sending a warning signal that has already pulled stock markets lower and, historically, has moved presidents to change course. The pressure is coming from two directions: uncertainty about whether oil prices will stay high because of the war with Iran, and deepening worry about the size and trajectory of U.S. government debt.

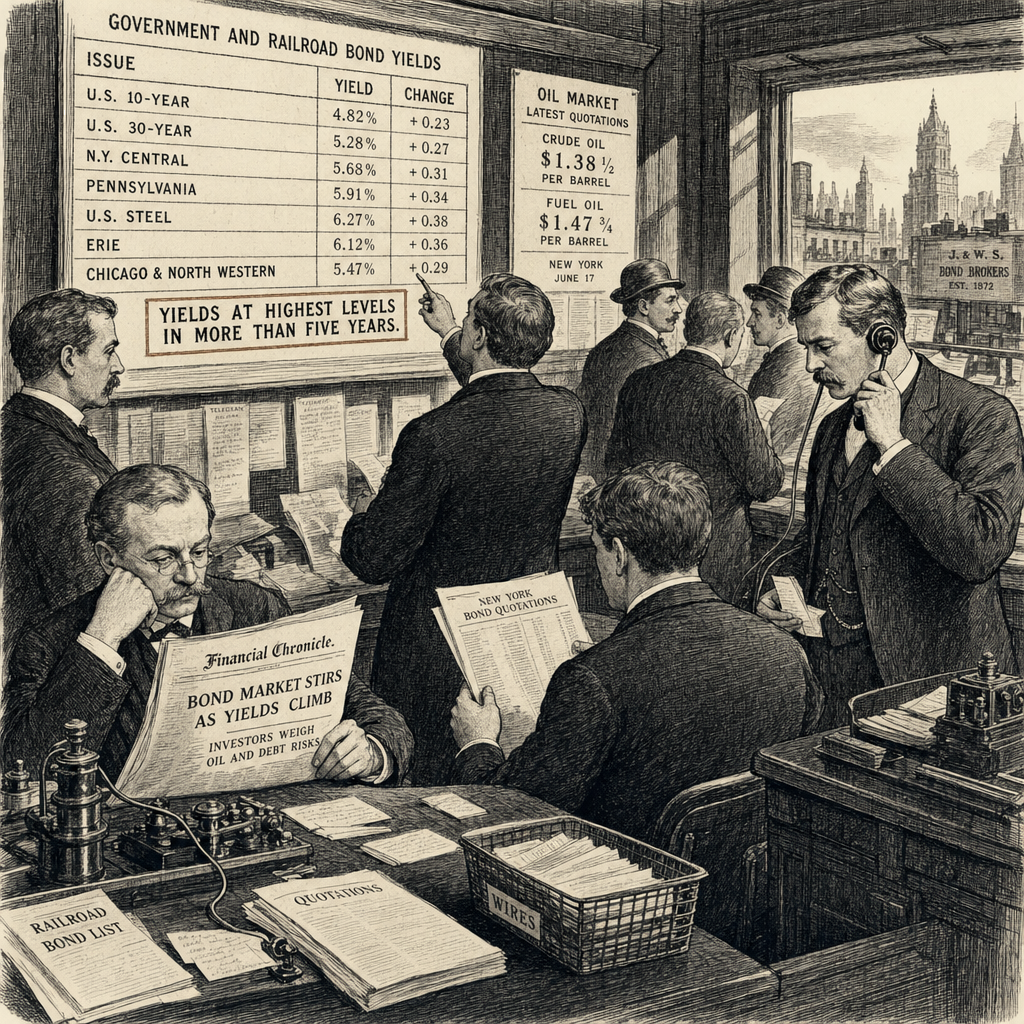

Global bond yields have been climbing steadily in recent weeks. The 10-year U.S. Treasury yield, a benchmark for borrowing costs around the world, has touched heights not reached since before the 2008 financial crisis, according to market data. Similar moves are underway in Europe, Japan, and other developed economies. The synchronized rise reflects a broad repricing of risk as investors demand higher compensation for holding long-term government debt.

Oil prices sit at the center of the bond market’s anxiety. The U.S.-Iran conflict, now in its second month, has kept crude elevated and injected uncertainty into forecasts for inflation and economic growth. Higher oil prices feed through to consumer prices, raising expectations that central banks will need to keep interest rates higher for longer. That dynamic pushes bond yields up. Economists and traders are watching for any sign of escalation or de-escalation in the conflict as a key driver of where yields go next.

Alongside oil, the size of the U.S. government’s debt load has become a growing focus for bond investors. The federal debt has swelled in recent years, and the cost of servicing it has risen as interest rates have climbed. The Congressional Budget Office has projected that debt held by the public will reach a record share of gross domestic product within the next few years. That trajectory has begun to worry bond buyers, who are demanding a higher “term premium” — the extra yield required to hold long-term debt over short-term debt.

Main Street Independent earlier today reported that bond market warning signals were rattling stocks and reshaping the White House’s risk calculus. Read the full earlier report.

The rising bond yields are already being felt in equity markets. The S&P 500 and other major indexes have fallen from their record highs set earlier this month, with interest-rate-sensitive sectors such as technology and real estate taking the heaviest losses. The Dow Jones Industrial Average has declined in four of the last five sessions. Investors are rotating out of stocks and into bonds as yields rise, a classic portfolio shift that intensifies selling pressure.

The bond market has a track record of exerting political influence that goes well beyond Wall Street. In the United Kingdom in 2022, a sudden surge in gilt yields forced the government of then-Prime Minister Liz Truss to reverse a set of unfunded tax cuts. In the United States, President Donald Trump has in the past adjusted policy positions when bond yields moved sharply — including backing off from trade escalation and other confrontational stances. The precedent is not lost on market participants or policymakers.

The current yield surge also threatens to slow the broader economy. Higher bond yields translate directly into higher mortgage rates, corporate borrowing costs, and government debt service payments. The housing market, already strained by elevated prices, faces a fresh headwind. Corporate investment plans may be delayed or canceled as financing costs rise. On the fiscal side, the Treasury will see its interest expense climb, potentially crowding out other spending and adding to the debt-cycle pressure that is itself a driver of higher yields.

The Federal Reserve has so far remained on hold with its benchmark interest rate, but the bond market’s move is doing some of the central bank’s work for it — tightening financial conditions without a rate change. Fed officials have noted in recent speeches that they are watching the bond market closely. If yields continue to climb, the central bank may face pressure to acknowledge the tightening and adjust its forward guidance.

Market strategists are divided on whether the current move represents a temporary spike or the beginning of a sustained regime of higher yields. Morgan Stanley’s chief U.S. equity strategist, Michael Wilson, has warned that the bond market’s message should not be ignored, pointing to the risk of a correction in stocks. Other analysts argue that if oil prices stabilize and the Iran situation de-escalates, yields could fall back. For now, the bond market has the floor — and it is speaking loudly.