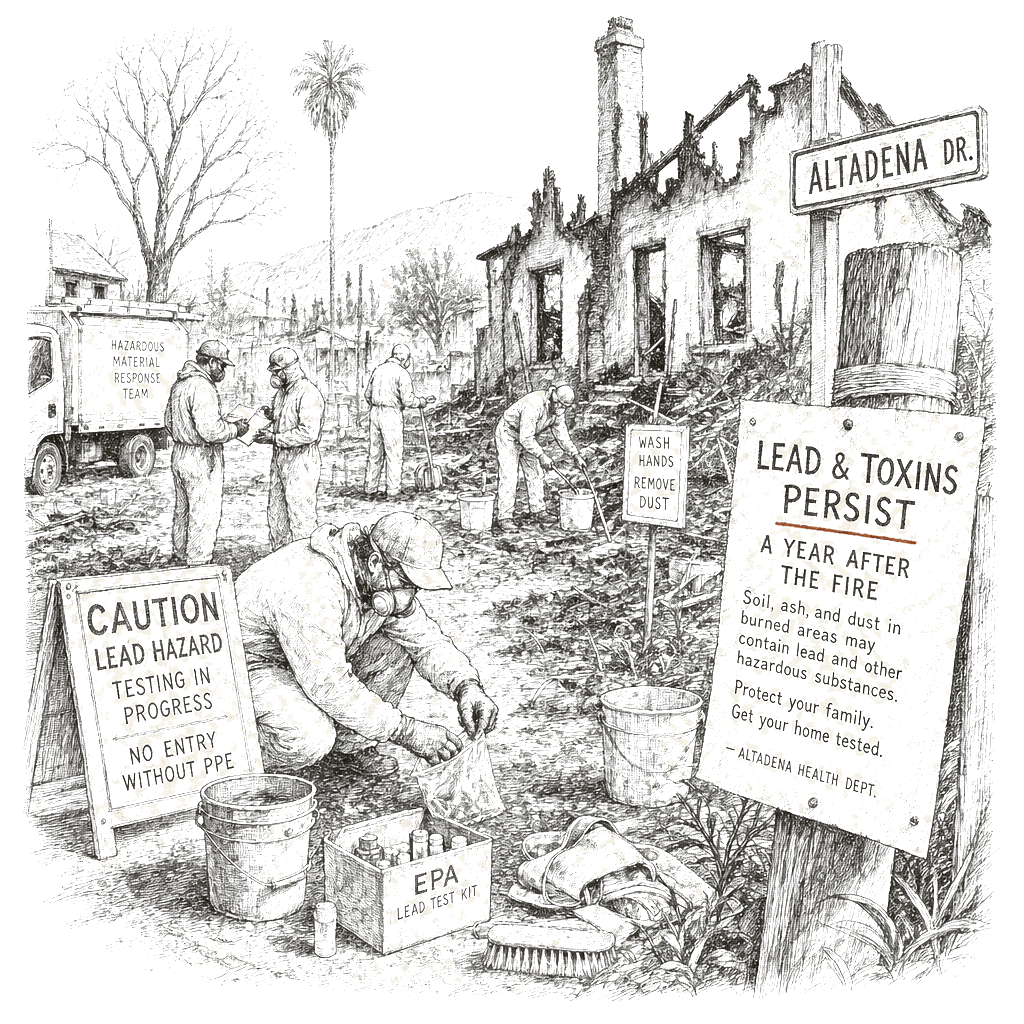

A year after the most destructive wildfires in Los Angeles area history scorched Altadena and Pacific Palisades, homeowners whose structures survived are confronting a continuing health crisis: lead, asbestos and other toxic compounds left behind by smoke and ash. Despite professional cleanings, six out of 10 smoke-damaged homes in the Eaton Fire area still show dangerous contamination levels, according to a November report by the volunteer group Eaton Fire Residents United. Many residents say their insurance companies are refusing to cover adequate testing and remediation, leaving families living in homes they fear may be harming them.

The fires that killed at least 31 people and destroyed nearly 17,000 structures on January 7, 2025, created a second wave of harm for survivors still inside contaminated homes — a hazard that public health experts say is understudied and that standard insurance policies often fail to address.

Dangerous levels persist after professional cleaning

The Eaton Fire Residents United report, released in November, drew on self-submitted data from 50 homeowners who had cleaned their homes, with 78% having hired professional cleaners. Of those 50 homes, 63% had lead levels above the Environmental Protection Agency’s standard, according to the report. Average lead levels were almost 60 times higher than the EPA’s rule.

The ash left behind by urban wildfires is, according to AP reporting, a toxic mixture of incinerated cars, electronics, paints, furniture and personal belongings. It can contain pesticides, asbestos, plastics, lead and other heavy metals. A recent study also found that volatile organic compounds from smoke — some known to cause cancer — lingered inside homes even after fires were extinguished.

The University of Southern California reported that more than 70% of homes within the Eaton Fire area were built before 1979, when lead paint was common, helping explain why lead has emerged as the dominant contaminant in surviving structures.

Families forced back into contaminated homes

Nina and Billy Malone considered their Altadena home of 20 years a safe haven before smoke, ash and soot seeped inside. Recent testing found harmful lead levels still on the wooden floors of their living room and bedroom even after professional cleaning. They were forced to move back in August after their insurance cut off rental assistance.

Since then, Nina said, she wakes up almost daily with a sore throat and headaches. Billy had to get an inhaler for worsening wheezing and congestion.

Their insurance company will not pay to retest the home, Billy said. They are considering paying $10,000 themselves. If results still show contamination, their insurer told them it would only pay to remediate federally regulated toxins like lead and asbestos — leaving unregulated compounds unaddressed.

“I don’t know how you fight that,” Nina said. “How do you find that argument to compel an insurance company to pay for something to make yourself safe?”

Children and pregnant residents face heightened risk

Zoe Gonzalez Izquierdo, who has children ages 2 and 4, said she cannot get her insurance company to pay for adequate cleanup of her family’s Altadena home, which tested positive for dangerous levels of lead and other toxic compounds.

“They can’t just send a company that’s not certified to just wipe things down so that then we can go back to a still contaminated home,” Gonzalez said.

Dr. Lisa Patel, a pediatrician and executive director of the Medical Society Consortium on Climate and Health, said eliminating lead exposure is especially urgent for pregnant individuals and young children.

“For individuals that are pregnant, for young children, it’s particularly important that we do everything we can to eliminate exposure to lead,” Patel said.

She said the same urgency applies to asbestos, because there is no safe level of exposure.

Insurance disputes compound the health burden

Residents in both Altadena and Pacific Palisades say they are largely at the mercy of their insurance companies, which decide what contamination they cover and how much remediation they will fund. California’s insurer of last resort, the California Fair Access to Insurance Requirements Plan, has faced scrutiny over its handling of fire damage claims.

Homeowners want state agencies to enforce an existing requirement that insurance companies restore a property to its pre-fire condition.

Julie Lawson said her family paid about $7,000 out of pocket to test soil at their Altadena home, even though their insurer had already agreed to pay to replace the grass in the front yard. They planned additional testing after finishing indoor remediation. If insurance would not cover it, Lawson said, they would pay for it themselves.

Even so, Lawson said the losses extend beyond contamination — including home equity and the community they had built over years.

“We have to live in the scar,” she said. “We’re all still really struggling.”

Mental health toll mounts

Annie Barbour, who works with the nonprofit United Policyholders and is herself a survivor of the 2017 Tubbs Fire in Northern California, said the experience of surviving with a standing home has carried its own particular anguish.

Many residents were at first relieved to see their houses still standing, Barbour said. “But they’ve been in their own special kind of hell ever since.”

Experts recommend that residents returning to smoke-exposed homes ventilate and filter indoor air by opening windows or running high-efficiency particulate air purifiers with charcoal filters. Residents handling ash or dust should wear gloves and respirators.

Nina Malone said she is considering therapy to cope with her anxiety. She continues to go through the couple’s belongings — clothes, dishes, boxes — one item at a time, wearing gloves and an N-95 mask, still finding soot and ash in cabinets and on floors.

“I don’t feel comfortable in the space,” she said.